You bought an audience. You got a screen.

The real cost of sport advertising in the streaming era — and the model nobody has built yet.

Hi there, the gold rush to sports right distribution is mad. Is really sport the new black in platforms era? Eng-Ita version and a useful TLDR down here. Let’s begin and thanks for following

There was a moment when buying a 30-second spot during a Serie A match on Sky felt like renting a table at the best restaurant in town. You weren’t buying an ad. You were buying membership.

I was there, inside Fox-Sky Italy. ‘Football like you’ve never seen it before’ wasn’t a tagline — it was a daily editorial promise. Cinematic direction. Commentators who’d turned play-by-play into performance art. Brands were guests, not interruptions. Cost per GRP: €11,000–13,000. Nobody complained. Nobody needed to.

Today, that world is gone. And here’s the punchline: on paper, the new world looks better for brands. More platforms. More inventory. Lower CPMs. Better metrics. More targeting. More data. More everything.

The metrics are excellent. But I argue that nobody is actually paying attention. That’s the paradox this article is about.

The race to the bottom dressed as progress

Over five years, every major platform decided live sport was the one thing worth overpaying for. Amazon: 1B/year for NFL Thursday Night Football. Google: 2B/year for NFL Sunday Ticket. Netflix: 5B over 10 years for WWE Raw, plus boxing, plus Christmas NFL. Apple TV+: exclusive global MLS. DAZN: 6.7 billion in equity burned by its founder, 9.8 billion in future rights commitments, and a 2024 revenue of 3.2B against rights costs of 3.1B+.

The rights arms race has a perverse outcome: the more platforms chase sport, the more ad inventory floods the market, and the lower CPMs fall. When Amazon launched its ad tier in early 2024 at ․24-25 CPM, it triggered a cascade. Netflix dropped from ․55 to ․37. Streaming CPMs fell 20–32% in twelve months.

The most expensive content in media history is producing the cheapest advertising inventory.

Four things are happening simultaneously that nobody in the room wants to put on a slide.

First: price falls, impact falls with it — context quality and CPM track together.

Second: these platforms were born on the promise of no ads. Spotify still says it out loud: upgrade if you want a better experience. The brand isn’t a guest. It’s the downgrade notification.

Third: On Netflix the no-ads plan doesn't protect viewers during live sports — ads reach everyone, including those who paid specifically not to see them. On DAZN there is no ad-free tier: you pay up to €70/month and the spots are there regardless. The brand doesn't interrupt someone who “didn't want to be disturbed”. It interrupts someone who already paid not to be disturbed. That's not advertising in a tolerated context. That's advertising in a context of active resentment.

Fourth: fragmentation across six to eight platforms destroys the collective ritual. Without shared ritual, there is no cultural moment. Without a cultural moment, the brand is buying a slot during someone else’s private appointment.

Sources — DAZN: Companies House UK 2024, Sportico; 2025 target ⁄5B: Insider Sport Oct 2025. CPM data: Ad Age 2024, Digiday. Bango Subscription Wars 2024, n=5,000 US subscribers: 78% believe paid subscriptions should never show ads; 71% of sports streaming subscribers leave or upgrade when ads appear.

The P&L that nobody frames on the wall

Sources — DAZN: Companies House UK 2024, Sportico. ESPN: Disney 10-K FY2024; Q3 FY2025: StreamTV Insider Aug 2025. YouTube ST: Morgan Stanley Research 2024. Sky UK: Comcast 2024; PL rights: Premier League Oct 2023. DAZN PIF investment ⁄1B: Sportcal Oct 2025. Netflix/Apple: Sportico/Bloomberg.

After fifteen years of disruption and twenty-plus billion dollars in losses, the streaming industry has successfully rebuilt the thing it was trying to kill: a hybrid subscription-plus-advertising model. The difference is that Sky built advertising as a premium context from day one. OTT platforms retrofitted it as an economic fix onto a product that had promised the opposite. The legacy of ‘ads = you couldn’t afford Premium’ doesn’t disappear because the CFO needs another revenue stream.

The gap nobody talks about: neither Sky nor the click

Here’s the structural problem with CTV sports advertising that gets papered over in every upfront presentation. It borrowed the format from the wrong era and the measurement promise from the wrong channel.

From linear broadcast it took the passive lean-back model: the 30-second spot, the mass interruption, the ‘sit there and watch it’ assumption. That was fine when the broadcaster had premium editorial exclusivity. The interruption happened inside a context the brand actually wanted to inhabit.

From digital it borrowed the promise of performance metrics. But not the thing that makes digital performance real: the click. On desktop, the attribution chain is closed — impression, click, conversion, done. On the living-room TV, that chain breaks. The remote doesn’t browse. QR code scan rates during live sports broadcasts sit at 1-3%. Companion apps lose 70-80% of users within thirty days.

CTV sports advertising: TV’s interruption model, without TV’s premium context. Digital’s measurement promise, without digital’s click. The worst of both worlds, sold as the best of both worlds.

The industry knows this. TripleLift’s 2026 report found that 49% of CTV campaigns still use 15 and 30-second formats designed for linear television. ‘Agencies are built to produce 15s and 30s,’ one executive admitted. Interactive formats — pause ads, overlays, shoppable experiences — are growing (engagement per impression nearly doubled year-on-year to 1.94% in Q2 2025) but remain a marginal experiment. YouTube is introducing ‘Peak Points’: AI that places your ad at the highest-attention moment during a cultural event. It’s progress. It’s still an interruption.

The only genuinely closed-loop exception is Amazon — with a precise perimeter. TNF 2025 viewers were 52% more likely to search for advertiser brands than other NFL audiences (EDO, 2026): that’s search lift, not direct purchase. And the loop only closes for brands that sell on Amazon. Critically, TNF spots are not built ad-hoc for the event — Amazon’s Audience-Based Creative technology serves different existing creatives to different segments, but the format is still the standard 30-second spot, identical to the one running on NBC or CBS. For automotive, insurance, luxury, or any brand without an Amazon storefront, the attribution chain breaks. Long-term brand recall on Prime Video sports remains publicly unmeasured. Completion rate: high. Active mental processing: not guaranteed.

So what are brands actually paying for? A TVision study published in the Journal of Advertising Research (September 2025), tracking second-by-second attention across 1,000+ viewers, found that CTV viewers pay less attention to ads than linear TV audiences — and that attention decays more steeply with each repetition on CTV than on linear. Repeat an ad six times and recall goes up 92%, per Nexxen research. But purchase intent drops 16% from the first to the sixth exposure. In a sports streaming context where frequency is high and the viewer is mentally locked onto the game, not the ad break, that decay curve is brutal.

The sports audience doesn’t ignore ads the way they scroll past a banner. They experience the interruption as a direct violation of the emotional contract they paid to enter. They came for the match. The ad is the price of not being able to afford the tier without one. That’s not attention. That’s hostage-taking. And brands are paying premium rates to be the hostage-taker.

Sources — CTV attribution gap: StreamLayer CTV Live Sports Guide 2026. TripleLift ‘Architecture of Attention’ 2026. Interactive CTV engagement: EMARKETER/BrightLine Q2 2025. Amazon closed loop: INCRMNTAL study 2025. CTV attention decay: Bhan & Rallabandi, Journal of Advertising Research, Sep 2025 (TVision Insights dataset). Ad repetition vs purchase intent: Nexxen research 2024-25, cited MNTN Research Feb 2026.

Gen Z doesn’t watch sport. They watch people watch sport.

43% of Gen Z prefers YouTube and TikTok to any form of television, including paid streaming. Only 31% of sports fans aged 18-24 watch full live matches, against 75% of over-55s. ESPN chairman Jimmy Pitaro has said the relationship with younger viewers is ‘the one thing that keeps me up at night.’ Not Amazon. Not Netflix. Creators.

This generation doesn’t want the institutional commentator reading from a press-box script. They want someone who reacts the way they react, who knows the same memes, who has a take before the referee has blown the whistle. The sports creator on YouTube with 300,000 subscribers who breaks down the formation with hand-drawn slides is not a lesser version of the Sky Studio. It’s a different product entirely — and for a specific audience, a better one.

The American lab: four case studies that aren’t theoretical

The US market has a five-year head start. These aren’t predictions — they’re current operating models with measurable results.

Pat McAfee built the most-watched sports show on YouTube — nearly 3 million subscribers, 3.4 billion X impressions in 2025. Aaron Rodgers announced career decisions live on McAfee’s show before talking to traditional media. ESPN then paid a multi-million dollar deal to license the show. Not hire McAfee. License him. He kept streaming on YouTube simultaneously. The power dynamic has permanently inverted: the broadcaster now pays the creator for access to his audience, not the other way around.

Amazon brought Dude Perfect — 60 million YouTube subscribers — as an alternative commentary stream for Thursday Night Football. Watch the game with traditional commentary or with creators. The result: TNF median viewer age dropped to 47, seven years below the NFL linear average. Same game, three simultaneous streams (classic commentary, creator layer, AI analytics). Three different audiences, three different brand integration opportunities, one event.

Bryson DeChambeau, two-time US Open champion, has 2.69 million YouTube subscribers. He invested over 1M building his own production company. His episode with Trump hit 13 million views. When his LIV Golf contract came up for renewal, he said going YouTube-only was ‘an incredibly viable option’. In April 2026 he co-founded Source Golf — a YouTube network aggregating creator content with centralised ad sales. The athlete is now a media company. The broadcaster needs him more than he needs the broadcaster.

The USGA invites YouTube golf creators to play its courses before the US Open. Lexus is the presenting sponsor: creators get a vehicle, caddies wear branded bibs, flags are co-branded. No spots. No interruptions. Lexus enters the narrative organically. Good Good Golf is valued at 45 million. Callaway treats them as creative co-directors, not sponsor recipients. This is the architecture for UEFA: federation provides access, creator brings audience, brand finances the ecosystem — near zero cost to the federation, global amplification as a by-product.

Sources — Pat McAfee: Stack Influence 2025; On3 2025; CAA Sports Media analysis. Dude Perfect/Amazon TNF: Barrett Media Oct 2023; SVG Oct 2022. DeChambeau: Golf.com Jan 2026; EssentiallySports May 2026; Awful Announcing Apr 2026. USGA/Good Good/Lexus: Digiday Sep 2025; PGA Tour Aug 2024.

YouTube: the only player with the maths to change everything

YouTube generated 60B in revenue in 2025 — more than Netflix (⁄45.2B). Ad revenue alone: 40.4B. Alphabet posted ⁄102B in one quarter. The Sunday Ticket costs 2B/year and loses 1.2B annually. Google absorbs it without blinking.

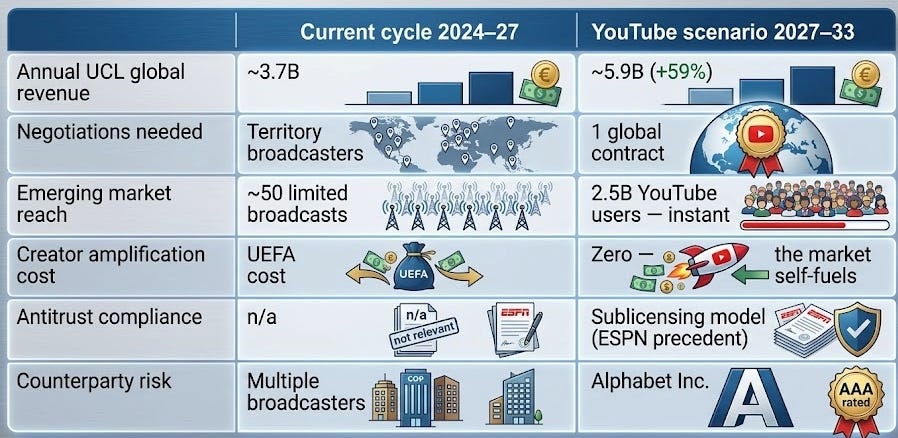

Let’s imagine it for one moment: YouTube acquires the 2027-2033 Champions League global rights (5.9B/year target per the ongoing Relevent negotiation) plus an international Serie A package (1.8B), total annual cost is around 7.7B — 19% of YouTube’s ad revenue. A loss, yes. A manageable strategic loss for the entity that controls the world’s largest advertising infrastructure and suddenly becomes the global home of football. Different from any bet DAZN or Apple ever made, because Google’s business model doesn’t need the sports rights to generate a direct return. The sports rights generate an ecosystem return — search, discovery, YouTube TV subscriptions, advertising data enrichment, 2.5 billion monthly users who now associate YouTube with football.

Sources — YouTube 2025: Variety Feb 2026. UEFA CL target: Goal.com/The Independent Oct 2025. ESPN sublicensing model: The Wrap Sep 2025. Alphabet Q3 2025: Variety Oct 2025. Sunday Ticket loss: Morgan Stanley Research 2024.

YouTube wouldn’t become Sky. It would become something Sky never was: an open platform where the live event, the creator commentary layer, and the free market of independent voices coexist on the same infrastructure. The Official Creator Roster — journalists-turned-publishers with exclusive locker room access, funded by UEFA as a condition of the rights deal — would replace the studio. The sports journalist doesn’t disappear. They become their own media company, their own brand, their own revenue stream. The broadcaster becomes the pipe. The creator becomes the experience.

What brands actually gain from this — and what they’ve been losing

The creator model solves the three structural failures of CTV sports advertising in one move.

Context: the brand doesn’t interrupt. It participates. The creator’s audience chose to be there. The brand is part of why they stay, not the reason they briefly look at their phone.

Attribution: the creator uses a promo code, a link in description, a swipe. The conversion chain is traceable without needing the TV remote to become a mouse. YouTube’s dynamic brand sponsorships — swappable slots in long-form creator videos, sold to different brands in different markets, with performance dashboards — give advertisers the equivalent of click-level data in a video-native format.

Receptivity: Magnite data shows 67% of live sports streamers pay more attention to ads aligned with their lifestyle and interests. The specialised sports creator is, by definition, interest-aligned. The audience isn’t resisting. They’re leaning in.

A seasonal creator partnership for a sports-specialist channel typically costs $25-50 CPM per thousand video views — comparable on paper to a standard CTV spot. But that unit of comparison is misleading. The creator CPM covers the full editorial context: the trust the audience has built with that creator over years, the narrative integration of the brand, the non-skippable nature of the endorsement and a conversion chain that is traceable through promo codes and links. You are not buying an impression. You are buying participation in a conversation. The Google/Circana MMM data confirms what that difference produces in the long run: 86% higher incremental ROAS than paid social, specifically for creator partnerships.

The cultural barrier is real and worth naming. European media managers do use creators and the industry is growing but still have KPIs built for GRP and linear CPM. Presenting a plan that swaps a ․15 CPM for an €80,000 seasonal creator partnership requires a metrics shift that most planning structures haven’t incorporated. This is the slowest change — and the most expensive one to delay. Because the brands that figure it out first will compound their advantage. The ones that don’t will keep financing the platforms’ rights deals in exchange for the efficient delivery of inattention.

Sources — CTV attribution gap: StreamLayer 2026; TripleLift ‘Architecture of Attention’ 2026. Interactive CTV: EMARKETER/BrightLine Q2 2025. Attention decay: Bhan & Rallabandi, Journal of Advertising Research Sep 2025. Creator partnership CPM: SponsorRadar H1 2025, Viral Nation 2025. Magnite live sports viewer data 2024. ROAS creator +86% long-term vs paid social: Circana MMM meta-analysis commissioned by Google (2025) — 40 MMM models, 10 US CPG brands, creator partnerships specifically — YouTube Creator Marketing Playbook Mar 2026. Distinct from Nielsen MMM (53,153 campaigns, 2022-2024) measuring YouTube AI ads (Demand Gen): +17% ROAS vs digital; YouTube +109% vs linear TV for retail (Google/Nielsen Social Study, 20 studies, 2020-2024). Amazon TNF 52% search lift: EDO Analytics, Amazon Ads Feb 2026. Amazon Audience-Based Creative: Amazon Ads documentation 2025.

The thesis

Sport is still the most powerful attention context in mass media. The streaming industry has spent a decade figuring out how to make that attention cheap, fragmented, and irritating to the people it’s trying to reach. Remarkable achievement.

The market has split into two incompatible worlds. The great mass events — Champions League finals, Olympics, Super Bowl — still work: collective ritual, premium context, brands as participants in a cultural moment. A handful per year, priced accordingly. The everyday match has become an ‘eventlet’: mediocre context, a viewer who paid to avoid exactly this, advertising as the tax on being unable to afford better.

YouTube is the only player with the financial scale, global reach, and advertising infrastructure to rebuild the architecture from scratch — not as a premium closed broadcaster, but as an open platform where live sport, creator commentary, and brand narrative coexist without the structural contradiction. The American examples — McAfee, Dude Perfect, DeChambeau, Good Good Golf — are not experiments. They are the operating model. They work. They scale. They generate measurable value for every party involved.

The brands that understand this first won’t just save money. They’ll own the conversation. Everyone else will keep paying to interrupt it.

TL;DR — IF YOU’RE IN A HURRY

→ Everyone is chasing sports rights. Costs go up. CPMs drop 20-32%. Looks like a win for brands. It isn’t.

→ Streaming platforms were born promising no ads. They added them when the economics broke. The viewer knows. The brand pays to be the symbol of the cheaper plan.

→ Netflix now shows ads during live sports even to no-ad subscribers. DAZN has no ad-free tier. This isn’t advertising in a tolerated context. It’s advertising in a context of active resentment.

→ CTV sports advertising borrowed the format from TV (passive 30-second spots) without the premium context, and the measurement promise from digital without the click. The worst of both worlds.

→ The only real exception is Amazon — but only for brands that sell on Amazon, and with standard spots not built for the event.

→ YouTube generates $60B in revenue annually — more than Netflix. It’s the only player that can buy Champions League rights without needing the sports economics to break even.

→ The model that changes everything: sports creators with exclusive event access, journalists becoming their own publishers, brands entering the narrative instead of interrupting it. Already operating in the US.

→Whoever figures this out first won’t just save on CPMs. They’ll own the conversation

_________________

Hai comprato un’audience.

Hai ottenuto uno schermo.

Il costo reale della pubblicità sportiva nell’era streaming — e il modello che nessuno ha ancora costruito in Europa.

di Emanuele Landi

C’era un momento in cui comprare uno spot durante una partita di Serie A su Sky era come prenotare un tavolo nel miglior ristorante della città. Non compravi uno spazio pubblicitario. Compravi un’appartenenza.

L’ho vissuto dall’interno, in Fox-Sky Italia. ‘Il calcio come non lo hai mai visto’ non era uno slogan: era un impegno editoriale mantenuto ogni domenica. Regie d’eccezione. Commentatori che avevano trasformato la telecronaca in arte. I brand erano ospiti, non interruzioni. Costo per GRP: €11.000–13.000. Nessuno protestava. Nessuno ne aveva bisogno.

Oggi quel mondo è scomparso. E la cosa curiosa è che, sulla carta, il nuovo mondo sembra migliore per i brand: più piattaforme, più inventario, CPM più bassi, metriche più precise, targeting chirurgico. Sembra un vantaggio competitivo.

Le metriche sono eccellenti. Nessuno sta davvero guardando. Questo è il paradosso di cui parla questo articolo.

La corsa al ribasso travestita da progresso

Negli ultimi cinque anni ogni grande piattaforma ha deciso che lo sport live è l’unica cosa per cui vale la pena strapagare. Amazon: 1 miliardo l’anno per il Thursday Night Football NFL. Google: 2 miliardi per il Sunday Ticket NFL. Netflix: 5 miliardi in dieci anni per il WWE Raw, più la boxe, più le partite di Natale. Apple TV+: MLS in esclusiva globale. DAZN: 6,7 miliardi di equity bruciati dal fondatore, 9,8 miliardi di impegni futuri su diritti, ricavi 2024 pari a 3,2 miliardi contro costi diritti di 3,1 miliardi.

Il risultato paradossale di questa gara al rialzo sui diritti è una gara al ribasso sui CPM. Quando Amazon ha lanciato il suo tier pubblicitario nel 2024 a 24-25 dollari ogni mille impression, ha scatenato un effetto domino: Netflix è scesa da 55 a 37 dollari. I CPM streaming sono calati del 20-32% in dodici mesi.

Il contenuto più costoso della storia dei media sta producendo l’inventario pubblicitario più economico.

Quattro cose stanno accadendo contemporaneamente che nessuno in sala vuole mettere su una slide. Prima: il prezzo scende, l’impatto scende con esso — qualità del contesto e CPM si muovono insieme. Seconda: queste piattaforme sono nate sulla promessa dell’assenza di pubblicità. Spotify lo dice ancora ad alta voce: passa a Premium se vuoi un’esperienza migliore. Il brand non è un ospite dell’evento: è la notifica di downgrade. Terza: e la cosa peggiore non è nemmeno questa. Su Netflix il piano no-ads non protegge lo spettatore durante gli eventi sportivi live — la pubblicità arriva comunque a tutti, anche a chi ha pagato per non vederla. Su DAZN non esiste un piano senza spot: si paga fino a 70 euro al mese e gli spot ci sono lo stesso. Il brand non interrompe chi ’non voleva essere disturbato’. Interrompe chi ha già pagato per non essere disturbato. Non è advertising in un contesto tollerato: è advertising in un contesto di risentimento attivo. Quarta: la frammentazione su sei-otto piattaforme distrugge il rito collettivo. Senza rito condiviso non esiste momento culturale. Senza momento culturale, il brand sta comprando uno slot durante l’appuntamento privato di qualcun altro.

Fonti — DAZN: Companies House UK 2024, Sportico; target 2025 5B$: Insider Sport ott 2025. CPM: Ad Age 2024, Digiday. Bango Subscription Wars 2024, n=5.000 abbonati US: 78% ritiene che i servizi a pagamento non debbano mostrare ads; 71% degli abbonati sport streaming abbandona o fa upgrade quando compaiono gli spot.

I conti che nessuno appende in cornice

Fonti — DAZN: Companies House UK 2024, Sportico. ESPN: Disney 10-K FY2024; Q3 FY2025: StreamTV Insider ago 2025. YouTube ST: Morgan Stanley Research 2024. Sky UK: Comcast 2024; diritti PL: Premier League ott 2023. Investimento PIF/DAZN 1B$: Sportcal ott 2025. Netflix/Apple: Sportico/Bloomberg.

Dopo quindici anni di disruption e venti miliardi di dollari in perdite, il settore streaming ha ricostruito con successo esattamente ciò che stava cercando di distruggere: un modello ibrido abbonamento più pubblicità. La differenza è che Sky aveva costruito la pubblicità come contesto premium fin dall’inizio. Le piattaforme OTT l’hanno innestata come correzione economica su un prodotto che aveva promesso l’esatto contrario. L’eredità psicologica — ‘la pubblicità è la penalizzazione per non aver scelto il piano migliore’ — non scompare perché il CFO ha bisogno di un’altra linea di ricavo.

Il gap che nessuno nomina: né Sky né il click

Il problema strutturale della CTV sportiva non è solo il contesto. È che ha preso il formato sbagliato da due mondi diversi senza ereditare il vantaggio di nessuno dei due.

Dal broadcast lineare ha preso il modello lean-back: lo spot da trenta secondi, l’interruzione passiva, il grande schermo in salotto. Questo era giustificabile quando il broadcaster aveva l’esclusiva editoriale. L’interruzione avveniva in un contesto che il brand voleva abitare.

Dal digital ha preso la promessa delle performance metrics. Ma non il suo asset fondamentale: il click. Su desktop la catena è chiusa — impressione, click, conversione, fatto. Sul televisore quella catena si spezza. Il telecomando non naviga. I QR code durante i live sportivi registrano scan rate tra l’1% e il 3%. L’app companion perde il 70-80% degli utenti entro trenta giorni.

Il CTV sportivo: il modello di interruzione della TV, senza il contesto premium della TV. La promessa di misurazione del digital, senza il click del digital. Il peggio di entrambi i mondi, venduto come il meglio di entrambi.

L’industria lo sa. Il report TripleLift 2026 ha rilevato che il 49% delle campagne CTV usa ancora i formati da 15 e 30 secondi progettati per la televisione lineare. Le agenzie sono costruite per produrre 15 e 30 secondi. I formati interattivi — pause ad, overlay, esperienze shoppable — stanno crescendo (il tasso di engagement per impression è quasi raddoppiato anno su anno al 1,94% nel Q2 2025) ma rimangono un esperimento marginale. YouTube sta introducendo i ‘Peak Points’: IA che posiziona lo spot nel momento di massima attenzione durante un evento. È progresso. È ancora un’interruzione.

L’unica vera eccezione è Amazon. I dati proprietari di prima parte permettono di collegare l’esposizione durante il Thursday Night Football a un acquisto successivo. Una ricerca INCRMNTAL su 2 miliardi di dollari di spesa ADV ha trovato che il CTV genera dieci volte più conversioni della TV lineare — dentro l’ecosistema chiuso di Amazon. Fuori da quell’ecosistema, sei di nuovo a reach, frequency e speranza. Si tratta di una sorta di supermercato retail dove il brand può vendere ma non costruire recall, bene per alcune categorie con sales veloce meno bene per altre.

Uno studio pubblicato sul Journal of Advertising Research nel settembre 2025 — basato sui dati secondo per secondo di TVision su oltre mille spettatori — ha dimostrato che su CTV l’attenzione decade più rapidamente di quanto non faccia sulla TV lineare a ogni ripetizione dell’ad. La ricerca Nexxen completa il quadro: la ripetizione aumenta il ricordo del 92% dopo sei esposizioni, ma l’intenzione d’acquisto scende del 16% dalla prima alla sesta. In un contesto sportivo streaming dove la frequenza è alta e lo spettatore è mentalmente altrove durante la pausa, quella curva di decadimento è brutale.

Il pubblico sportivo non ignora gli spot come scorre oltre un banner. Vive l’interruzione come una violazione diretta del contratto emotivo per cui ha pagato. È lì per la partita. Lo spot è il prezzo per non aver potuto permettersi il tier senza.

Fonti — Gap attributivo CTV: StreamLayer CTV Live Sports Guide 2026. TripleLift ‘Architecture of Attention’ 2026. Interactive CTV: EMARKETER/BrightLine Q2 2025. Amazon ecosistema chiuso: INCRMNTAL 2025. Decadimento attenzione CTV: Bhan & Rallabandi, Journal of Advertising Research, set 2025 (dataset TVision Insights). Ripetizione vs intenzione d’acquisto: Nexxen research 2024-25, citato MNTN Research feb 2026.

La Gen Z non guarda lo sport. Guarda persone che guardano lo sport.

Il 43% della Gen Z preferisce YouTube e TikTok a qualsiasi forma di televisione, incluso lo streaming a pagamento. Solo il 31% dei fan sportivi tra i 18 e i 24 anni guarda le partite integrali in diretta, contro il 75% degli over 55. Jimmy Pitaro, chairman di ESPN, ha detto che il rapporto con i consumatori più giovani è ‘l’unica cosa che mi tiene sveglio la notte’. Non Amazon. Non Netflix. I creator.

Questa generazione non vuole il telecronista istituzionale che legge dalla tribuna stampa. Vuole qualcuno che reagisce come reagirebbe lei, che conosce gli stessi meme, che ha un’opinione prima che l’arbitro abbia fischiato. Il creator sportivo su YouTube con 300.000 iscritti che smonta la formazione con slide disegnate a mano non è una versione inferiore dello Studio Sky. È un prodotto diverso — e per un’audience specifica, migliore.

Il laboratorio americano: quattro casi che non sono teoria

Il mercato americano ha cinque anni di vantaggio sull’Europa. Non sono previsioni: sono modelli già in funzione con risultati misurabili.

Pat McAfee ha costruito su YouTube il programma sportivo più visto della piattaforma — quasi 3 milioni di iscritti, 3,4 miliardi di impression su X nel 2025. Aaron Rodgers ha annunciato le sue decisioni di carriera in diretta sulla sua trasmissione prima di comunicarle ai media tradizionali. Nel 2023 ESPN ha pagato un accordo multimilionario per licenziare il suo show — non per assumerlo, per licenziarlo. McAfee continua a trasmettere in parallelo su YouTube. La direzione del potere si è invertita definitivamente: non è il broadcaster che sceglie il commentatore, è il creator che sceglie chi gli conviene distribuire.

Amazon Prime Video ha portato Dude Perfect — 60 milioni di iscritti YouTube — come broadcaster alternativo per il Thursday Night Football. Il ‘TNF with Dude Perfect’ è uno stream parallelo alla partita: gli spettatori scelgono tra la telecronaca classica o quella dei creator. Risultato demografico: l’età mediana del TNF è scesa a 47 anni, sette anni sotto la media NFL lineare. Amazon offre simultaneamente tre stream diversi sullo stesso evento: telecronaca classica, creator commentary, analisi AI in tempo reale. Tre layer, tre audience, tre opportunità di brand su un unico match.

Bryson DeChambeau, due volte campione degli US Open, ha 2,69 milioni di iscritti YouTube. Ha investito oltre un milione di dollari costruendo la propria società di produzione. Il suo episodio con Trump ha raggiunto 13 milioni di views; quello con Steph Curry 16,5 milioni. Quando si è discusso del rinnovo con LIV Golf, ha detto che vivere di solo YouTube e giocare i major era ‘un’opzione incredibilmente percorribile’. Nell’aprile 2026 ha fondato Source Golf con altri creator — una rete YouTube con vendita pubblicitaria centralizzata. L’atleta non ha più bisogno del broadcaster per avere un’audience. Il broadcaster ha bisogno dell’atleta.

L’USGA invita i creator YouTube a giocare sui suoi percorsi nei giorni precedenti gli US Open. Lexus è il presenting sponsor: i creator ricevono un veicolo, i caddie indossano divise con logo US Open, i flag sono brandizzati. Nessuno spot. Nessuna interruzione. Il brand entra nella narrazione in modo organico. Good Good Golf vale 45 milioni di dollari. Callaway li tratta come co-direttori creativi, non come semplici sponsor. Questa è l’architettura per UEFA: federazione che fornisce accesso, creator che porta audience, brand che finanzia l’ecosistema — costo per la federazione quasi zero, amplificazione globale come effetto collaterale gratuito.

Fonti — Pat McAfee: Stack Influence 2025; On3 2025; analisi CAA Sports Media. Dude Perfect/Amazon TNF: Barrett Media ott 2023; SVG ott 2022. DeChambeau: Golf.com gen 2026; EssentiallySports mag 2026; Awful Announcing apr 2026. USGA/Good Good/Lexus: Digiday set 2025; PGA Tour ago 2024.

Lo scenario YouTube: l’unico player con i numeri per cambiare tutto

YouTube ha generato 60 miliardi di dollari di ricavi nel 2025 — più di Netflix (45,2 miliardi). Il solo ad revenue vale 40,4 miliardi l’anno. Alphabet ha registrato 102 miliardi di fatturato in un singolo trimestre del 2025. Il Sunday Ticket costa 2 miliardi l’anno e perde 1,2 miliardi: Google lo assorbe senza battere ciglio.

Se UEFA prezzasse il ciclo Champions League 2027-2033 a 5,9 miliardi l’anno — come emerge dalle trattative in corso con l’agenzia Relevent — e YouTube lo acquisisse insieme a un pacchetto di diritti internazionali Serie A da altri 1,8 miliardi, il costo totale sarebbe intorno a 7,7 miliardi annui. Pari al 19% del solo ad revenue YouTube. Una perdita enorme in valore assoluto. Gestibile come investimento strategico nell’ecosistema più grande della storia del broadcasting: Google Ads più YouTube più 2,5 miliardi di utenti mensili attivi che improvvisamente cercano e guardano calcio sulla stessa piattaforma dove guardano tutto il resto.

YouTube non diventerebbe Sky. Diventerebbe qualcosa che Sky non poteva essere: una piattaforma aperta dove il live, il layer creator e il libero mercato delle voci indipendenti coesistono sulla stessa infrastruttura. Il roster ufficiale di creator — giornalisti sportivi che diventano editori di se stessi, creator affermati con accrediti esclusivi UEFA — rimpiazzerebbe lo studio. Il giornalista sportivo non sparisce: diventa la propria società di media, il proprio brand, il proprio flusso di ricavo. Il broadcaster diventa il tubo. Il creator diventa l’esperienza.

Cosa guadagnano davvero i brand — e cosa hanno perso fin qui

Il modello creator economy sportiva risolve i tre fallimenti strutturali della CTV sportiva standard in un colpo solo.

Contesto: il brand non interrompe. Partecipa. L’audience del creator ha scelto di essere lì. Il brand è parte del motivo per cui restano, non la ragione per cui guardano il telefono.

Attribuzione: il creator usa un codice promozionale, un link in descrizione, uno swipe. La catena di conversione è tracciabile senza che il telecomando diventi un mouse. I dynamic brand sponsorship di YouTube — slot swappabili nei video long-form, vendibili a brand diversi per mercati diversi, con dashboard di performance — danno agli advertiser dati equivalenti al click, in formato video-native.

Ricettività: i dati Magnite mostrano che il 67% degli spettatori di sport in streaming presta più attenzione agli spot allineati ai propri interessi. Il creator sportivo specializzato è, per definizione, allineato agli interessi. L’audience non respinge: si sporge in avanti.

Una partnership stagionale con un creator sportivo specializzato costa tipicamente $25-50 CPM per mille view del video — comparabile sulla carta a uno spot CTV standard. Ma l’unità di misura è fuorviante. Il CPM del creator include il contesto editoriale completo: la fiducia che l’audience ha costruito con quel creator nel corso degli anni, l’integrazione narrativa del brand, la natura non-skippabile dell’endorsement e una catena di conversione tracciabile attraverso promo code e link. Non stai comprando un’impression. Stai comprando la partecipazione a una conversazione. I dati Google/Circana MMM confermano cosa produce quella differenza nel lungo periodo: un ROAS incrementale superiore dell’86% rispetto al paid social, specificatamente per le creator partnership.

La barriera culturale è reale e vale la pena nominarla. I responsabili media europei usano molto i creator e siamo di fronte ad una industria crescente, ma hanno ancora i KPI calibrati su GRP e CPM lineari. Presentare un piano che sostituisce un CPM da 15 dollari con una creator partnership da 80.000 euro per stagione richiede un cambio di metriche che le strutture decisionali non hanno ancora incorporato. Questo è il cambiamento più lento — e il più costoso da ritardare. Perché i brand che lo capiscono per primi non risparmieranno soltanto: possederanno la conversazione. Gli altri continueranno a finanziarla.

Fonti — Gap attributivo CTV: StreamLayer 2026; TripleLift 2026. CTV interattivo: EMARKETER/BrightLine Q2 2025. Decadimento intenzione d’acquisto: Nexxen/MNTN Research feb 2026. Intenzione d’acquisto creator +40%: Spiralytics Creator Economy Report 2025. ROAS creator +86% long-term vs paid social: Google/Circana MMM meta-analysis, 53.153 campagne, 104 settimane, 2022-2024 (YouTube Blog mar 2026; Nielsen MMM commissionato da Google, 2024). Magnite sport streaming viewer data 2024.

La tesi

Lo sport è ancora il contesto di attenzione più potente che esista nella comunicazione di massa. Il settore streaming ha trascorso un decennio a capire come rendere quell’attenzione economica, frammentata e irritante per le persone che cerca di raggiungere. Risultato notevole.

Il mercato si è spaccato in due mondi incompatibili. I grandi eventi di massa — finali di Champions, Olimpiadi, Super Bowl — funzionano ancora: rito collettivo intatto, contesto premium, brand come partecipanti a un momento culturale. Pochi all’anno, prezzati di conseguenza. La partita quotidiana è diventata un ‘eventino’: contesto mediocre, uno spettatore che ha pagato per evitare esattamente questo, la pubblicità come tassa sull’incapacità di permettersi di meglio.

YouTube è l’unico player con la scala finanziaria, la distribuzione globale e l’infrastruttura ADV per ricostruire l’architettura da zero — non come broadcaster premium chiuso, ma come piattaforma aperta dove lo sport live, il creator commentary e la narrazione di brand coesistono senza la contraddizione strutturale. Gli esempi americani — McAfee, Dude Perfect, DeChambeau, Good Good Golf — non sono esperimenti. Sono il modello operativo. Funzionano. Scalano. Generano valore misurabile per tutte le parti.

I brand che lo capiscono per primi non risparmieranno soltanto sui CPM. Possederanno la conversazione. Tutti gli altri continueranno a pagare per interromperla.