Why Everyone Wants to Buy Warner Bros. Discovery?

t’s Not About Content — It’s About Economic Stability

Benvenuti a questo nuovo appuntamento di approfondimento. Come di consueto in doppia versione: prima inglese poi sotto in italiano. 3 minuti di lettura. Let’s go!

If there’s one word that defines today’s media industry, it’s overproduction.

Endless content. Collapsing attention spans. Hype that burns out in a weekend.

AI accelerates everything — more formats, more sameness, more noise.

In this chaos, a simple distinction reveals the pattern:

Content is consumed.

IP accumulates.

And content IP is not “a story.”

IP is economic infrastructure.

This is why everyone wants Warner Bros. Discovery.

“Netflix isn’t buying Warner for content.

It’s buying time — and time is the real margin in the new media economy.”

1. The nuance almost no one is seeing: content vs. cultural IP

Netflix is phenomenal at generating global hits — Stranger Things, Wednesday, Squid Game —

but these hits share two fragile traits:

they create spikes, not foundations

they don’t survive generational cycles

Warner is the opposite.

Harry Potter, DC, Looney Tunes, Game of Thrones, The Lord of the Rings —

these are cultural institutions, not editorial products.

👉 Netflix makes waves. Warner owns the tides.

2. IP isn’t content — it’s a cultural operating system

A cultural IP is something that:

lives across generations

encodes emotion

becomes a language

expands transmedially

outlasts trends

powers licensing, retail, entertainment, and experiences

stabilizes a platform’s economics

AI can create a story.

AI cannot create a multi-generational sense of belonging.

IP is the last moat left in entertainment — and it compounds over time if a brave publisher is ready to innovate and capitalize on it.

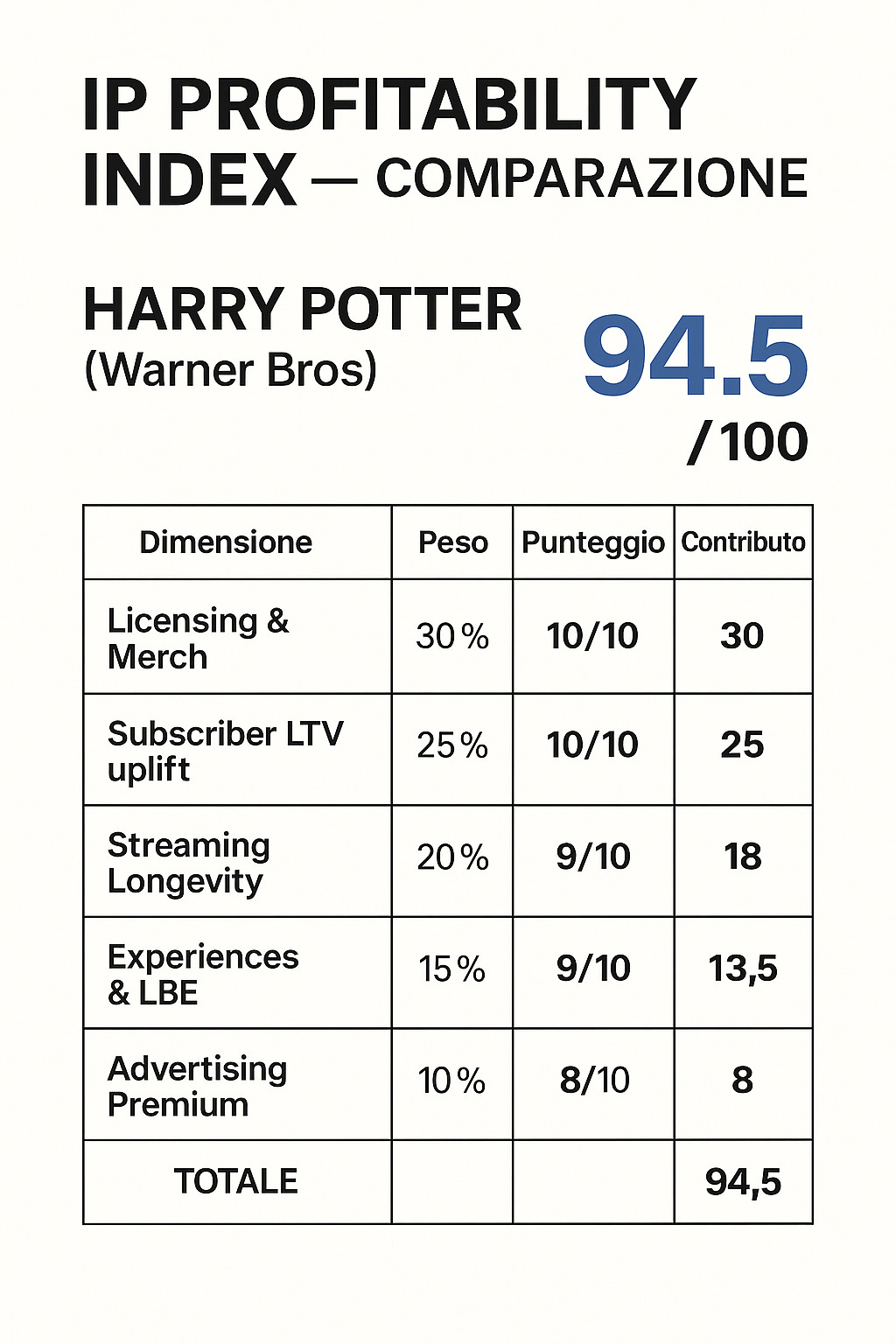

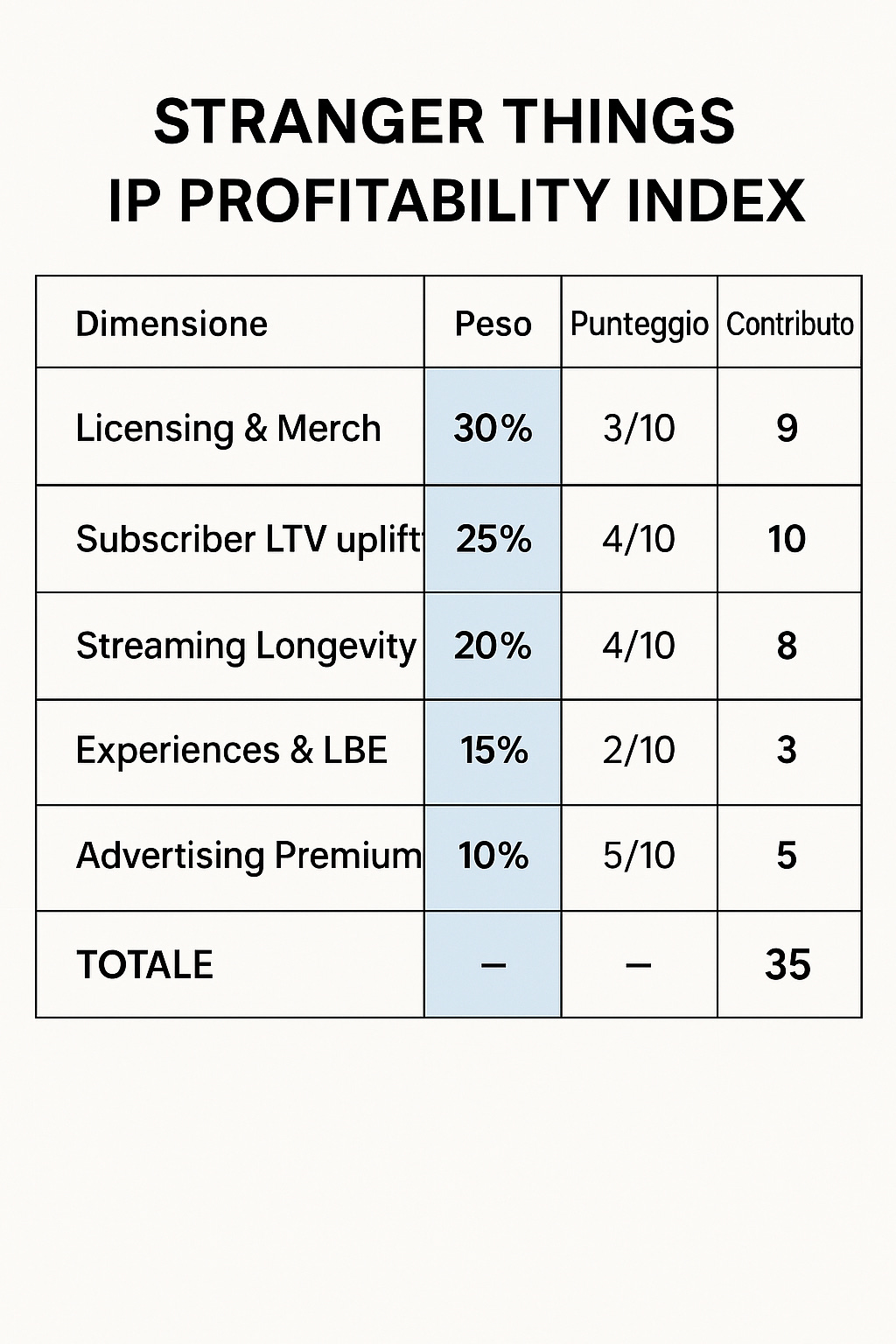

3. The IPI — IP Profitability Index

To separate “hits” from “heritage,” I created a simple, readable index and I applied it to two of the most impactful Ips of Netflix and Warner Bros - Stranger Things and Harry Potter.

IPI — IP Profitability Index, combining five variables:

Licensing & Merchandising

Subscriber LTV uplift

Streaming longevity

Experiences & LBE

Advertising premium

Results:

Harry Potter: 94.5 / 100

Stranger Things: 35 / 100

i weighted per single dimension of the profit according to business practice of profitability.

Netflix owns phenomena. Warner owns cities.

4. LTMC — Long-Term Marginality Contribution

In order to find a way to model the economic impact of cultural IP across decades I tried to create an acronim, a simple term: long term marginality contribution

LTMC is a simulated metric — not a financial disclosure — designed to express the long-term margin contribution of a stable, multi-platform IP.

Formula:

LTMC = Annual Margin × (IPI / 100) × Years × Derisk Factor (1–1.5–2)

For Harry Potter (conservative scenario):

Annual margin: $480–670M *

IPI: 0.945

Horizon: 20 years

👉 Conservative LTMC: $9–13B

👉 Intermediate LTMC: $13–19B

Expanded across the entire Warner IP ecosystem:

👉 Total LTMC: $25–65B

Significant — but still not enough to “pay for the acquisition.”

And that is precisely the point:

IP doesn’t pay for the deal.

IP enables the economic model that pays for the deal.

* Derived from open data and market practice across licensing, experiences, publishing, and gaming.

5. The deal logic everyone is missing:

Netflix + Warner ≈ 400M global subscribers

This is the number that changes everything.

Not because of scale

because of pricing power.

6. The real financial engine: ARPU uplift × scale

To be clear: this is not a forecast.

It’s an illustrative way to show the order of magnitude that even a small price change unlocks when applied to a subscriber base approaching 400 million.

Scenario: +€1/month

€1 × 400M subs × 12 months ≈ €4.8B in additional annual revenue.

Undiscounted, if Netflix managed to sustain an average uplift of around €1/month on a ~400M base over a decade, that would translate into roughly €48B in cumulative incremental revenue.

Not as a guaranteed stream — but as a realistic sense of scale.

Scenario: +€1.5/month

€1.5 × 400M × 12 ≈ €7.2B/year

→ order-of-magnitude impact: €70B over ten years (undiscounted)

Scenario: +€2/month

€2 × 400M × 12 ≈ €9.6B/year

→ order-of-magnitude impact: €95–100B over ten years (undiscounted)

These numbers are not meant to imply stable pricing or perfect retention over 20 years.

They serve one purpose:

to demonstrate the economic power of ARPU leverage when a platform controls cultural IP strong enough to sustain price elasticity without triggering churn.

Netflix’s churn has historically remained among the lowest in the industry (≈2%), which makes even modest price adjustments disproportionately valuable over long horizons.

This—not the size of the catalog, nor the raw subscriber count—is the true financial logic behind the interest in Warner’s IP ecosystem.

7. The four additional value pillars no one talks about

1. Content cost reduction

Netflix spends ~$17B/year on content.

A 10–15% efficiency gain = $30–50B saved over 20 years.

2. Advertising premium uplift

IP-backed environments increase CPMs.

Even +$1 CPM → multi-billion uplift.

3. Experiences, retail & location-based entertainment

Netflix House × Warner IP = a scalable physical entertainment business.

4. Risk transformation

Strong IP improves margin predictability and enhances the financial risk profile of the platform.

8. Why this is different from past acquisitions

Netflix is:

a mature platform

with a profitable core

global distribution

superior product & UX

real pricing leverage

Netflix wouldn’t be buying nostalgia.

It would be buying the foundation of its future economics.

9. What this means for brands

If IP is the most stable asset in a volatile content economy,

brands must stop acting like broadcasters

and start acting like cultural architects.

A brand without IP is fragile.

A brand with IP enters the economy of durability.

And that’s where the Decalogue comes in.

⭐ DECALOGUE — How to Turn a Brand Into a Cultural Asset

1. Stop thinking in “content.” Think in “cornerstones.”

An IP is not a campaign. It is a worldview.

2. Choose a timeless human theme.

Something bigger than your product.

3. Create a character, not a format.

Characters are sticky. Formats expire.

4. Invest as if you were building a theme park, not a post.

IP requires worldbuilding, naming, codes, symbols, multi-year narratives.

If it’s free to make, it’s not IP.

5. Commit to a 3–5 year horizon.

IP is not “real-time marketing.” It is commitment.

6. Expand across touchpoints.

IP becomes valuable only when it becomes everywhere.

7. Co-create with your community.

You don’t manage IP — you evolve it together.

8. Measure the IP, not the content.

Use LTV uplift, cultural memorability, narrative retention, community depth, associative equity.

9. Ask: could this IP be monetized beyond communication?

If not, it’s a tactic — not an IP.

10. Remember the golden rule: IP requires capital.

Stability costs — but instability costs far more.

11. Accept the role of luck.

J.K. Rowling didn’t know Harry Potter would become a cultural institution.

Serendipity is part of every IP origin story.

_________________

Se c’è una parola che definisce l’industria dei media di oggi, è iperproduzione.

Contenuti infiniti. Attenzione che crolla. Hype che dura un weekend.

L’AI accelera tutto — più formati, più omologazione, più rumore.

In questo caos, una distinzione semplice rivela il modello:

👉 Il contenuto viene consumato.

Le IP si accumulano.

E le IP non sono “una storia.”

Sono infrastruttura economica.

Ecco perché tutti vogliono Warner Bros. Discovery.

“Netflix non vuole comprare Warner per i contenuti.

Vuole comprare tempo — e il tempo è il vero margine nella nuova economia dei media.”

1. La sfumatura che quasi nessuno vede: contenuto vs. IP culturali

Netflix è straordinaria nel generare hit globali — Stranger Things, Wednesday, Squid Game —

ma queste hit condividono due tratti fragili:

creano picchi, non fondamenta

non sopravvivono ai cicli generazionali

Warner è l’opposto.

Harry Potter, DC, Looney Tunes, Game of Thrones, Il Signore degli Anelli —

sono istituzioni culturali, non prodotti editoriali.

👉 Netflix crea onde. Warner possiede le maree.

2. Le IP non sono contenuti — sono sistemi operativi culturali

Una IP culturale è qualcosa che:

attraversa generazioni

codifica emozione

diventa un linguaggio

si espande transmedialmente

supera le tendenze

alimenta licensing, retail, entertainment ed esperienze

stabilizza l’economia di una piattaforma

L’AI può creare una storia.

L’AI non può creare un senso di appartenenza transgenerazionale.

Le IP sono l’ultimo “moat” rimasto nell’entertainment — e capitalizzano nel tempo se c’è un editore abbastanza coraggioso da innovarle e sfruttarle.

3. L’IPI — IP Profitability Index

Per distinguere “hit” da “heritage”, ho creato un indice semplice e leggibile,

applicandolo a due delle IP più impattanti di Netflix e Warner Bros:

Stranger Things e Harry Potter.

IPI — IP Profitability Index, basato su cinque dimensioni:

Licensing & Merchandising

Uplift di LTV dell’abbonato

Longevità in streaming

Esperienze & LBE

Advertising premium

Risultati:

Harry Potter: 94.5 / 100

Stranger Things: 35 / 100

Ho pesato ogni dimensione secondo la prassi di profittabilità delle major.

👉 Netflix possiede fenomeni. Warner possiede città.

4. LTMC — Long-Term Marginality Contribution

Per modellare l’impatto economico delle IP culturali lungo i decenni,

ho introdotto un acronimo semplice: Long Term Marginality Contribution.

È una metrica simulata — non un dato finanziario — pensata per esprimere il contributo di margine a lungo termine di una IP stabile e multipiattaforma.

Formula:

LTMC = Margine Annuale × (IPI / 100) × Anni × “Derisk Factor” (1–1,5–2)

Per Harry Potter (scenario conservativo):

Margine annuale: $480–670M *

IPI: 0,945

Orizzonte: 20 anni

👉 LTMC conservativo: $9–13B

👉 LTMC intermedio: $13–19B

Estendendo la matematica a tutto l’ecosistema Warner:

👉 LTMC totale: $25–65B

Significativo — ma non sufficiente a “pagare l’acquisizione.”

Ed è proprio questo il punto:

Le IP non pagano il deal.

Abilitano il modello economico che paga il deal.

* Stima ricavata da open data e prassi industriale per licensing, esperienze, publishing e gaming.

5. La logica dell’operazione che tutti stanno perdendo di vista

Netflix + Warner ≈ 400 milioni di abbonati globali

Questo è il numero che cambia tutto.

Non per la scala.

Per il potere di pricing.

6. Il vero motore finanziario: ARPU uplift × scala

Chiariamo: non è una previsione.

È un modo per capire l’ordine di grandezza che anche un piccolo aumento di prezzo genera quando applicato a ~400 milioni di utenti.

Scenario: +1€/mese

1€ × 400M × 12 ≈ 4,8 miliardi €/anno

Su 10 anni, non scontati: ≈ 48 miliardi €

Non come flusso garantito — ma come scala potenziale.

Scenario: +1,5€/mese

1,5€ × 400M × 12 ≈ 7,2 miliardi €/anno

→ ordine di grandezza: 70 miliardi € su 10 anni

Scenario: +2€/mese

2€ × 400M × 12 ≈ 9,6 miliardi €/anno

→ ordine di grandezza: 95–100 miliardi € su 10 anni

Questi numeri non implicano stabilità dei prezzi o retention perfetta.

Servono a mostrare una cosa:

👉 il potere economico dell’ARPU quando la piattaforma possiede IP abbastanza forti da sostenere l’elasticità di prezzo senza far esplodere il churn.

Il churn storico di Netflix (~2%) è tra i più bassi del settore,

e rende anche piccoli aumenti estremamente preziosi su orizzonti lunghi.

Questo — non la dimensione del catalogo — è il vero razionale finanziario dietro l’interesse per l’ecosistema IP di Warner.

7. Le quattro leve aggiuntive di valore di cui nessuno parla

1. Riduzione dei costi di contenuto

Netflix spende ~17B$ l’anno.

Efficienza 10–15% → 30–50B$ risparmiati in 20 anni.

2. Advertising premium uplift

Le IP aumentano il CPM.

Anche +1$ di CPM → impatti da miliardi.

3. Experiences, retail & location-based entertainment

Netflix House × Warner IP = un business fisico scalabile.

4. Trasformazione del rischio

Le IP forti aumentano la prevedibilità del margine

e migliorano il profilo di rischio finanziario della piattaforma.

8. Perché questa operazione è diversa da quelle del passato

Netflix è:

una piattaforma matura

con un core profittevole

distribuzione globale

UX superiore

vero pricing power

Netflix non comprerebbe nostalgia.

Comprerebbe le fondamenta della sua economia futura.

9. Cosa significa per i brand

Se le IP sono l’asset più stabile nella content economy,

i brand devono smettere di agire da broadcaster

e iniziare ad agire da architetti culturali.

Un brand senza IP è fragile.

Un brand con IP entra nell’economia della durabilità.

E qui entra in gioco il Decalogo.

⭐ DECALOGO — Come trasformare un brand in un asset culturale

1. Smettila di pensare in “contenuti”. Pensa in “fondamenta”.

Una IP non è una campagna — è una visione del mondo.

2. Scegli un tema umano senza tempo.

Qualcosa più grande del prodotto.

3. Crea un personaggio, non un formato.

I personaggi durano. I formati scadono.

4. Investi come se stessi costruendo un theme park, non un post.

Worldbuilding, naming, codici, simboli, narrazioni pluriennali.

Se è gratis da fare, non è una IP.

5. Orizzonte 3–5 anni.

La IP non è real-time marketing. È commitment.

6. Espandi su ogni touchpoint.

La IP diventa preziosa solo quando diventa ovunque.

7. Co-crea con la community.

Le IP non si gestiscono, si evolvono.

8. Misura la IP, non il contenuto.

Usa LTV uplift, memorabilità culturale, retention narrativa, profondità comunitaria, equity associativa.

9. Chiediti: può essere monetizzata oltre la comunicazione?

Se no, è una tattica — non un’IP.

10. Ricorda la regola aurea: le IP richiedono capitale.

La stabilità costa. L’instabilità costa molto di più.

11. Accetta il ruolo della fortuna.

J.K. Rowling non sapeva che Harry Potter sarebbe diventato una istituzione culturale.

La serendipità è parte di ogni origine IP.