Why Brands Should worry if TV abdicates to YouTube

The quality of attention is at stake

Another week, another gig for my english - italian followers and subscribers here and on Peaklight. Here you have both language version of my take

Un’altra settimana, un’altro giro di giostra per i miei followers e abbonati qui e su Peaklight. Qui in entrambe le lingue la versione del mio pezzo.

Enjoy and thanks for following.

The year 2026 marks a tipping point for those who control advertising budgets. The strategic agreements between France Télévisions, BBC, and YouTube are not merely distribution headlines; they represent a genetic mutation of the value the medium offers to brands. If linear TV accepts being a mere content provider for the global “tube,” it is abdicating its primary function: acting as the guardian of brand equity.

Beyond the ocean, brilliant minds like Alan Wolk claim that “YouTube is TV” due to interface superiority and the capacity to drive new audiences, while Evan Shapiro prophesies the victory of the Creator Economy. Fascinating theories, but in Europe, they risk becoming a self-fulfilling prophecy only if we succumb to structural inertia.

Building on my work with international industry hubs, it’s clear that the challenge isn’t technological—it’s about value. For a brand, lasting sales are the result of building three fundamental pillars: Credential Capital, Social Capital, and Cultural Capital.

1. Credential Capital: Beyond the Performance Trap

Credential capital is about function: what the product is for and why to buy it now. This is the realm of “performance,” where YouTube and Walled Gardens dominate with immense volumes at low costs. But sales that endure do not thrive on clicks alone. If a brand invests only here, it becomes a commodity. A TV industry that chases digital volumes on their own turf, selling off inventory, offers brands a tactical fix that fails to build strategic value.

2. Social Capital: TV as the Arena of Collective Trust

Social capital is collective legitimacy: the value derived from the fact that “everyone knows that brand is relevant.” Linear TV, with its moments of shared viewing—from national events to cult fiction—is the only medium capable of creating a common arena.

Europe already has fandoms; they are intergenerational and rooted. But if broadcasters abdicate distribution, they weaken the “social glue” that makes a brand a safe, shared choice rather than just an isolated algorithmic suggestion.

3. The Asset of Cultural Capital

Cultural capital is identity: it is when a brand becomes a symbol. This is built only in high-prestige, curated editorial environments. YouTube seeks out broadcasters precisely because it hungers for their cultural capital. If a brand settles for being distributed anywhere without caring about the environment, it erodes its own prestige.

The Thesis: Certifying Attention Equity

The challenge for the market is about measuring value. We must stop counting heads and start certifying Attention Equity. We don’t need to outrun the tech giants on interface; we need to outclass them on contact quality.

We must impose the Q-GRP (Quality GRP) as a native trading metric:

Intrinsic Measurement: JICs must certify real contact quality (Completion rate, AVOC, immersiveness) as a native pricing variable.

Non-negotiable Value: If a publisher guarantees a high-attention, low-dispersion environment, the brand is purchasing social capital, not just “noise.”

European Federation: This is the only way to offer brands the necessary scale to compete with Walled Gardens while protecting the cultural identity of our markets.

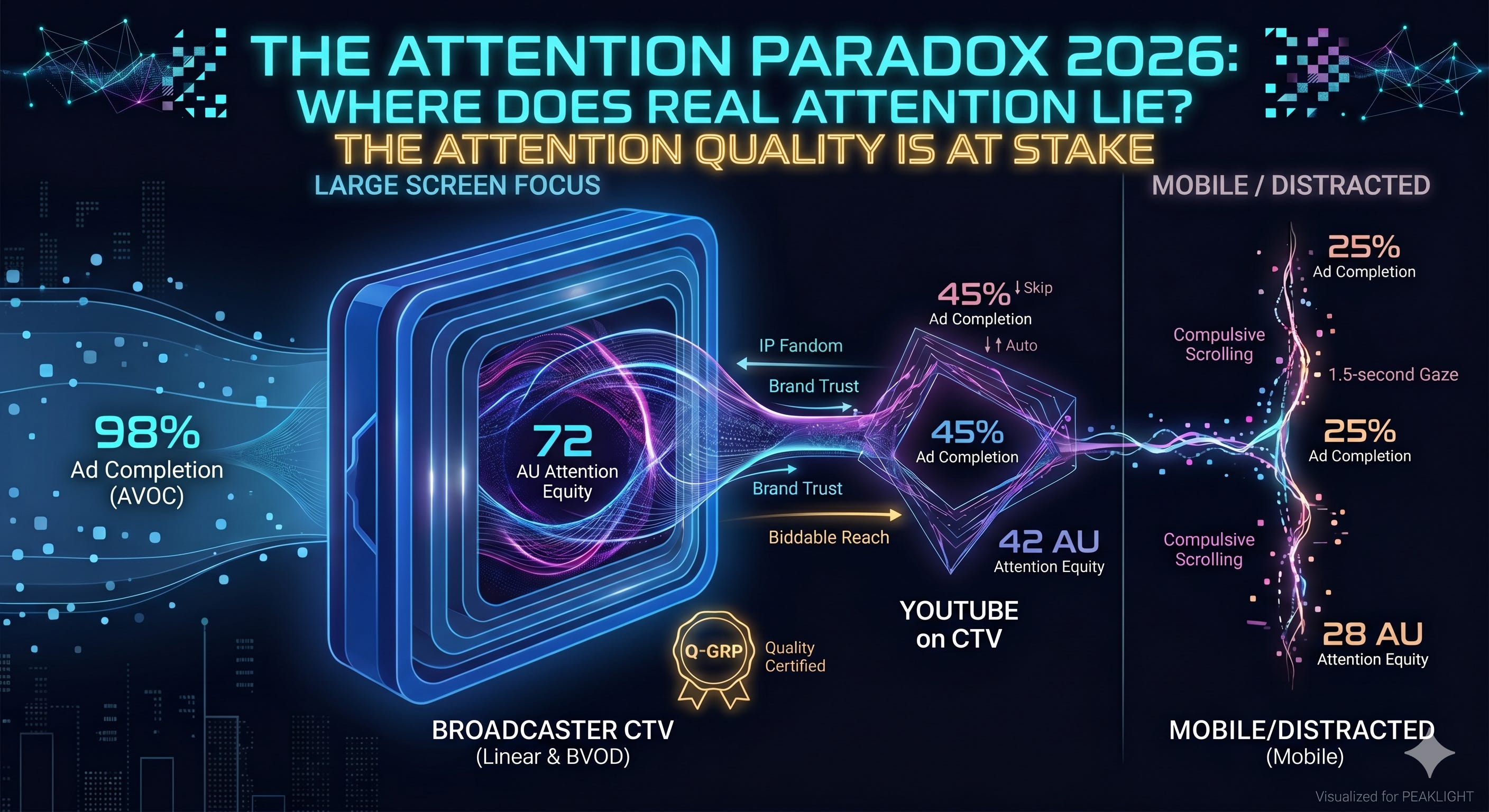

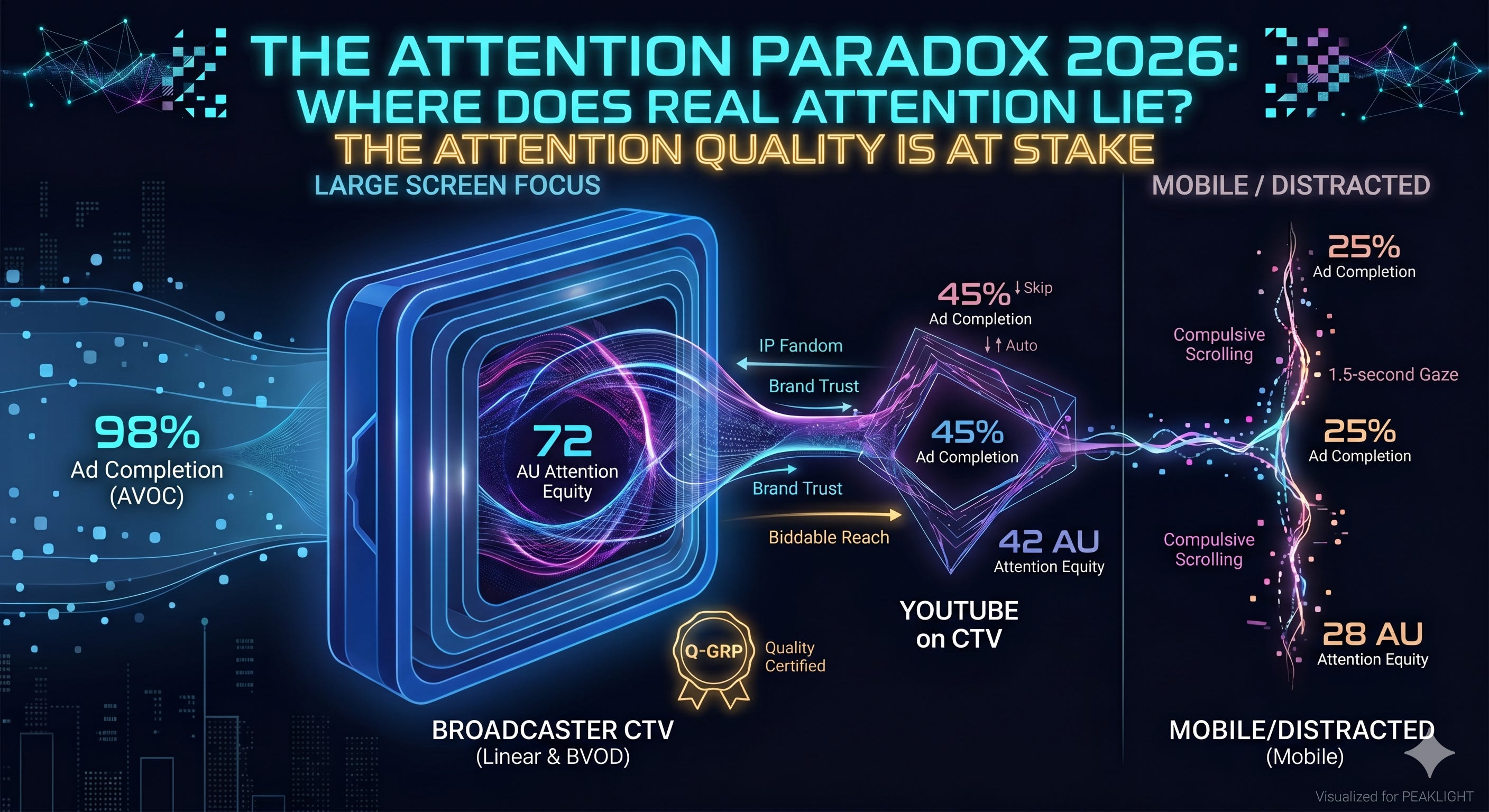

This data art demonstrates to CMOs that while YouTube (even on CTV) offers fragmented attention, a Broadcaster provides a solid core of Attention Equity that directly fuels their three brand capitals.

Source: Market benchmarks derived from public studies by Lumen Research, TVision, and industry effectiveness reports (2025-2026).

In Conclusion

Brands should not seek the lowest price, but the most solid value. If linear TV limits itself to becoming a passive provider, brands lose their most important stage. The challenge for CMOs today is not just “being there,” but being present where attention is a guaranteed, certified asset.

______________________

Perché i Brand dovrebbero preoccuparsi se la TV abdica a YouTube?

di Emanuele Landi

Il 2026 segna un punto di rottura per chi sposta i budget pubblicitari. Gli accordi strategici tra France Télévisions, BBC e YouTube non sono semplici esperimenti di distribuzione: rappresentano una mutazione genetica del valore che il mezzo offre alle marche.

Se la TV lineare accetta di essere un semplice fornitore di contenuti per il “tubo” globale, sta abdicando alla sua funzione primaria: quella di garante dei capitali di marca.

Oltreoceano, menti brillanti come Alan Wolk sostengono che ‘YouTube sia ormai la TV’ grazie alla sua superiorità d’interfaccia, mentre Evan Shapiro profetizza la vittoria della Creator Economy. Tesi affascinanti, che però in Europa rischiano di trasformarsi in una profezia che si autoavvera solo se decidiamo di soccombere all’inerzia strutturale.

Per un brand, la vendita stabile e duratura non è un atto impulsivo, ma il risultato della costruzione di tre pilastri fondamentali che oggi rischiano di essere erosi da un’eccessiva frammentazione distributiva: il capitale credenziale, il capitale sociale e il capitale culturale.

1. Il Capitale Credenziale: Oltre la trappola della pura performance

Il capitale credenziale riguarda la funzione: a cosa serve il prodotto e perché comprarlo ora. È il terreno della “performance”, dove YouTube e i Walled Garden dominano con volumi immensi a basso costo. Ma la vendita che resiste nel tempo non si nutre di soli clic. Se un brand investe solo qui, diventa una commodity. La TV che rincorre i volumi digitali sul loro stesso campo, svendendo inventario, offre ai brand una soluzione tattica che non costruisce valore strategico.

2. Il Capitale Sociale: La TV come arena della fiducia collettiva

Il capitale sociale è la legittimazione collettiva: il valore che deriva dal fatto che “tutti sanno che quel brand è rilevante”. La TV lineare, con i suoi momenti di visione condivisa — dai grandi eventi nazionali alle fiction di culto — è l’unico mezzo capace di creare un’arena comune. Abdicare alla distribuzione significa indebolire quel “collante sociale” che rende un brand una scelta sicura e condivisa, trasformandolo in un’opzione algoritmica isolata in un feed personalizzato.

3. L’asset del Capitale Culturale

Il capitale culturale è l’identità: quando un brand diventa un simbolo. Questo si costruisce solo in ambienti ad alto prestigio e contesti editoriali curati. YouTube cerca i broadcaster proprio perché ha fame del loro capitale culturale. Se il brand si accontenta di essere distribuito ovunque senza curare l’ambiente, erode il proprio prestigio nel lungo periodo.

La tesi: Certificare l’Attention Equity

La sfida per il mercato non è tecnologica, ma di misurazione del valore. Come ho sostenuto nel mio recente contributo per egta nel report “ad pricing models and strategies for multiplatform tv companies”, dobbiamo smettere di contare le teste e iniziare a certificare l’Attention Equity.

Dobbiamo imporre il Q-GRP (Quality GRP) come metrica nativa di trading:

Misurazione Intrinseca: I JIC devono certificare la qualità reale del contatto (Completion rate, AVOC, immersività) come variabile nativa del pricing.

Valore non negoziabile: Se un editore garantisce un ambiente ad alta attenzione e bassa dispersione, il brand sta acquistando capitale sociale, non semplice “rumore”.

Federazione Europea: È l’unico modo per offrire ai brand la massa critica necessaria per competere con i Walled Garden, proteggendo l’identità culturale dei nostri mercati.

Questa opera di data art dimostra ai CMO che, mentre YouTube (persino su CTV) offre un’attenzione frammentata, il Broadcaster garantisce un nucleo solido di Attention Equity in grado di alimentare direttamente i tre capitali di marca.

Fonte: Benchmark di mercato derivati da studi pubblici di Lumen Research, TVision e report sull’efficacia del settore (2025-2026).

In conclusione

I brand non devono cercare il prezzo più basso, ma il valore più solido. Se la TV lineare si limita a diventare un fornitore passivo di piattaforme terze, i brand perdono il loro palcoscenico più importante. La sfida per chi sposta i budget oggi non è “esserci”, ma essere presenti dove l’attenzione è un asset garantito e certificato.