The battle for the new attention infrastructure

Are AI chatbots the next OTT platforms?

Welcome to this new analysis of my bi weekly newsletter and greetings to my intl. reader on Peaklight. As always my newsletter will be in double languange: English and italian. (italian version below).

In the late 1990s, competition wasn’t between websites.

It was between browsers.

Netscape and Internet Explorer didn’t produce content.

They didn’t entertain anyone.

They simply decided where the internet started.

Whoever owned the browser owned the entry point.

And whoever owned the entry point quietly controlled everything else.

Then it happened again.

Social networks didn’t just become publishing tools — they became the infrastructure of time spent.

Then streaming did the same for video.

And now, something similar is happening again.

This time, with AI chatbots.

From tools to infrastructure

ChatGPT, Gemini, Claude or Copilot are often described as assistants.

But that framing is misleading.

They’re not tools anymore.

They’re becoming places.

Inside a single conversation you can:

research products

summarize documents

write briefs

analyze data

plan campaigns

prepare presentations

A growing share of cognitive work now starts there.

And wherever work and attention move, business eventually follows.

This isn’t about “running ads inside ChatGPT.”

It’s simpler than that.

If decisions start there, media planning comes later.

It’s the same dynamic we saw with Google Search twenty years ago.

First intent.

Then inventory.

Follow the money (not the hype)

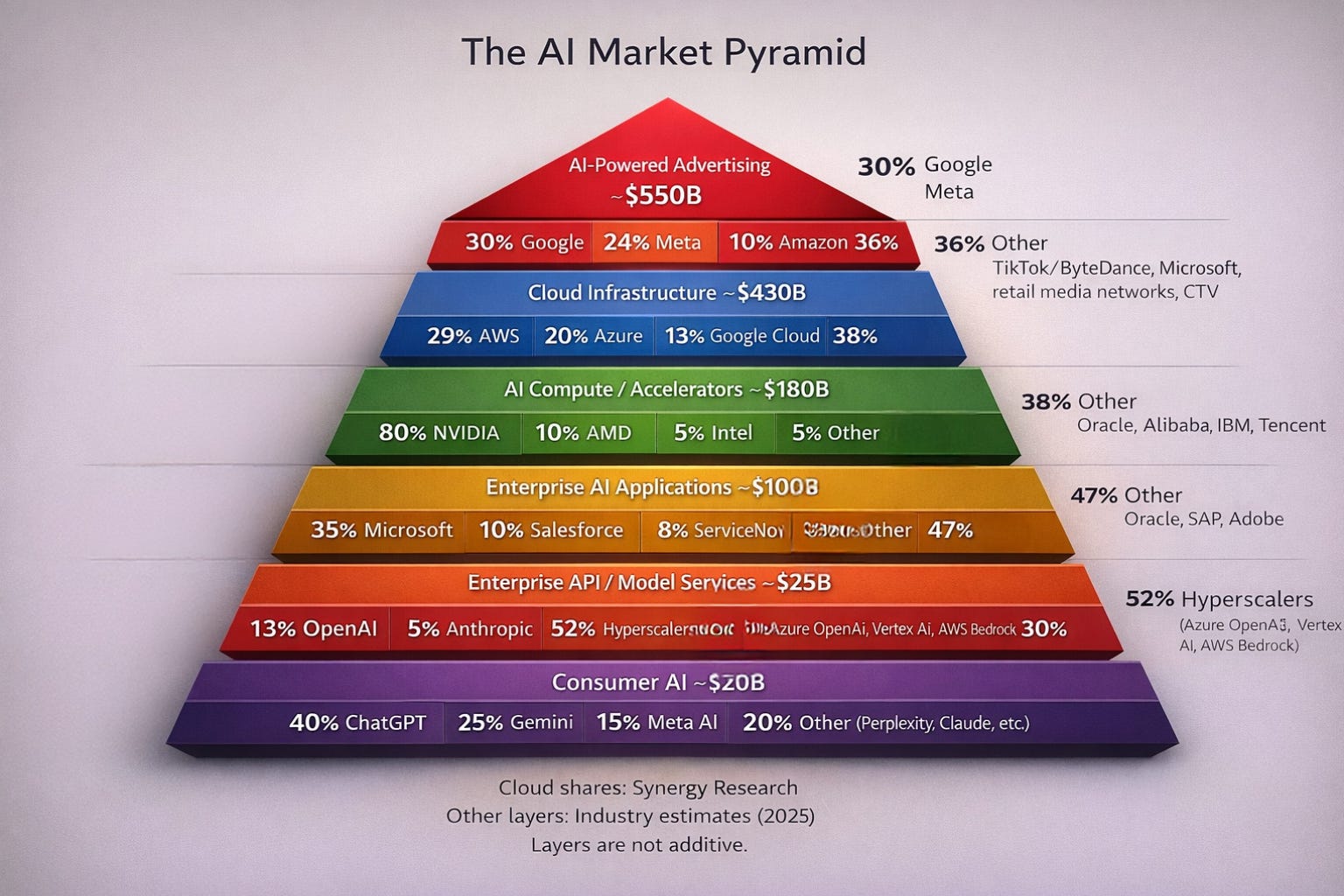

If you step back and look at the economics, the picture becomes clearer.

📊 The AI economy, 2025 (approx.)

Digital advertising: ~$550B

Cloud infrastructure: ~$430B

AI compute (GPUs/accelerators): ~$180B

Enterprise AI applications: ~$100B

Enterprise API / model services: ~$20–25B

Consumer AI subscriptions: ~$20B

The most talked-about segment — models and chatbots — is actually the smallest.

Most of the value sits underneath:

cloud, hardware, and media.

Interfaces attract attention.

Infrastructure captures margins.

Where power actually concentrates

Once you map the stack, the dynamics are almost obvious.

NVIDIA sells the energy

AWS, Azure and Google sell the factories

Model providers sell intelligence

Chatbots are simply the interface

Most enterprises don’t buy “AI” from a startup.

They buy cloud consumption.

A large share of OpenAI usage in production flows through Azure.

The model may be OpenAI’s.

The invoice is Microsoft’s.

Historically, distribution beats pure technology.

Netscape is still the best reminder.

If chatbots are the new browsers, APIs are the new AWS.

And NVIDIA is the power plant.

The real shift: media, software and work merging

The big change isn’t just better models.

It’s structural.

Media, tools and infrastructure are collapsing into the same interface.

Inside one environment you can:

watch

write

analyze

plan

decide

The boundary between consumption and production is fading.

It’s a hybrid space — part browser, part office, part search engine, part media channel.

When too many things start happening in the same place, that place becomes strategic.

What this means in practice

Beyond demos and experimentation, the implications are operational.

Not theoretical.

Data beats content volume

Chatbots don’t read storytelling.

They read structured information.

Clean knowledge bases and organized data determine whether you show up in the answer or disappear entirely.

AI becomes infrastructure, not a marketing toy

If it supports customer care, reporting or planning, it belongs in the core tech stack.

Not in an innovation lab.

Automate processes, not creativity

Analysis, synthesis and repetitive cognitive work deliver the highest ROI.

Freeing up human time matters more than generating cheap assets.

Discovery changes

More decisions will start inside a conversation, not just a search engine.

Being understandable to models becomes almost as important as buying media.

Systems > campaigns

Competitive advantage shifts from one-off initiatives to permanent architecture.

Less “big launch.”

More “always-on systems.”

Closing thoughts

Every digital era had its invisible infrastructure:

the browser

the feed

streaming

Conversation is next.

Chatbots won’t replace everything — nothing ever does.

But they will increasingly become the place where decisions start.

And when decisions move, markets follow.

First the interface changes.

Then the business does.

For those who arrive late, it always feels sudden.

Sources

Synergy Research (cloud market share)

IDC & Gartner (AI/GenAI enterprise spending)

eMarketer / IAB (digital advertising)

Public company disclosures and industry estimates

La battaglia per la nuova infrastruttura dell’attenzione

I chatbot AI sono i nuovi OTT?

Alla fine degli anni ’90 la competizione non era tra siti web.

Era tra browser.

Netscape e Internet Explorer non vendevano contenuti. Non producevano informazione. Non facevano intrattenimento. Semplicemente decidevano da dove iniziava internet.

Chi controllava il browser controllava l’accesso. E chi controllava l’accesso controllava tutto il resto.

Poi è successo di nuovo.

I social network non erano solo piattaforme di publishing. Sono diventati l’infrastruttura del tempo speso. Facebook e Instagram non hanno sostituito i media tradizionali: hanno spostato le ore delle persone altrove.

Poi è arrivato lo streaming. Netflix, YouTube, Prime Video. Non canali, ma ambienti chiusi dove contenuto, distribuzione, dati e pubblicità convivevano nello stesso posto.

Ogni volta lo schema è simile. Prima una tecnologia. Poi un’abitudine. Poi un’infrastruttura.

Quando qualcosa diventa infrastruttura, il business si riorganizza intorno a quel punto.

Oggi quella trasformazione sta avvenendo con i chatbot AI.

Non sono tool. Sono luoghi

ChatGPT, Gemini, Claude, Copilot non sono solo assistenti più veloci.

Stanno diventando ambienti operativi dove si lavora e si decide.

Dentro una conversazione oggi si cercano prodotti, si sintetizzano ricerche, si scrivono brief, si analizzano dati, si pianificano campagne, si preparano presentazioni. Inizia a succedere lì dentro una parte crescente del lavoro cognitivo.

E dove si sposta il lavoro, si sposta anche l’attenzione.

Il punto non è “fare advertising dentro ChatGPT”.

È molto più semplice: se la decisione nasce lì, la pianificazione media arriva dopo.

È la stessa logica che abbiamo visto con Google vent’anni fa. Prima l’intenzione, poi l’inventory.

Seguire i soldi aiuta a capire meglio

Se si guarda l’economia dell’AI con un minimo di distacco dall’hype, l’immagine è meno futuristica e più concreta.

Nel 2025 il valore dei diversi layer si distribuisce più o meno così:

Advertising digitale: ~$550 miliardi

Cloud infrastructure: ~$430 miliardi

AI compute (GPU e acceleratori): ~$180 miliardi

Enterprise AI applications: ~$100 miliardi

Enterprise API / modelli generativi: ~$20–25 miliardi

Consumer AI (abbonamenti e app): ~$20 miliardi

La parte di cui si parla di più — modelli, API, chatbot — è la più piccola in termini economici.

La fetta grande è sopra: cloud, hardware e soprattuto advertising,

Infrastruttura o Advertising ?

Guardando la filiera si capisce meglio dove si sta concentrando il potere. Al momento è tutto concentrato sull’advertising perché genera i volumi maggiori consolidati in anni di volumi di audience social e li l’AI è un abilitatore, un ottimizzatore. E’ fatturato a breve termine, ecco perché Chat GPT prova a prendere un pezzo di quella torta inserendo l’adv nel tier gratuito (esattamente come fanno alcuni operatori OTT), ma attenzione a sfidare i colossi con sistemi altamente integrati.

Se il fatturato a breve termine lo porta senz’altro la pubblicità, l’infrastruttura determina quel fatturato nel lungo periodo ed ha meno concorrenza: Nvidia vende l’energia: le GPU che rendono possibile tutto il resto.

AWS, Azure e Google vendono le fabbriche: l’infrastruttura dove l’AI gira davvero.

OpenAI e Anthropic vendono i modelli.

I chatbot sono l’interfaccia.

Molte aziende pensano di comprare “intelligenza artificiale”. In realtà stanno comprando consumo cloud.

Gran parte dei modelli OpenAI utilizzati in produzione passa da Azure. Il modello è di OpenAI, ma la fattura è di Microsoft.

Storicamente vince chi controlla la distribuzione enterprise, non chi ha soltanto la tecnologia migliore. Netscape è un buon promemoria.

I prossimi mercato che potrebber esplodere nella piramide sono quelli del gpu (servirà più potenza), i cloud (servirà più storage), enterprise AI application (le aziende aumenteranno il ricorso ad applicazioni AI man mano che impareranno a gestirla)

Media, software e lavoro stanno collassando nello stesso spazio

La novità vera non è la qualità dei modelli, che continuerà a migliorare come tutte le tecnologie. È il fatto che media, strumenti di lavoro e infrastruttura stanno convergendo nella stessa interfaccia.

Dentro una chat puoi guardare un contenuto, scrivere una mail, analizzare un dataset, chiedere un piano media, generare una creatività. Non c’è più distinzione netta tra consumo e produzione.

È uno spazio ibrido. Un po’ browser, un po’ CRM, un po’ search engine, un po’ ufficio.

Quando troppe cose iniziano ad accadere nello stesso posto, quel posto diventa strategico.

Cosa significa, in pratica, per chi lavora nei media e nel marketing

Al di là delle demo e degli esperimenti, le implicazioni sono molto operative.

Serve meno enfasi su “fare contenuti con l’AI” e più attenzione a come si costruiscono i sistemi.

Prima di tutto contano i dati. Le chatbot non leggono storytelling: leggono basi dati, cataloghi strutturati, knowledge base, informazioni pulite. Chi è organizzato viene citato nelle risposte, chi non lo è sparisce.

Poi c’è il tema infrastrutturale. Se l’AI entra in customer care, media planning, reporting o sales, non è più un tool di marketing ma un pezzo dello stack IT. Va trattata come investimento strutturale, non come test.

L’automazione ha senso sui processi ripetitivi — analisi, sintesi, reportistica, RFP — più che sulla creatività. Liberare tempo operativo crea valore più di generare creatività a caso.

Infine, cambia la discovery. Una parte crescente delle decisioni inizierà in una conversazione. Non solo su Google. Questo rende la “leggibilità” da parte dei modelli quasi importante quanto la presenza media.

In un contesto del genere, il vantaggio competitivo non nasce tanto dalla campagna migliore, ma dall’organizzazione migliore.

Meno iniziative spot. Più sistemi permanenti.

In chiusura

Ogni epoca digitale ha avuto la sua infrastruttura invisibile: il browser, il feed, lo streaming.

La conversazione è la prossima.

I chatbot non sostituiranno tutto, come non lo ha fatto nessuna tecnologia prima. Ma diventeranno il luogo dove iniziano sempre più decisioni. E quando le decisioni si spostano, il mercato segue.