Rented attention is a melting asset. I know. I lost mine.

Why the slow-built brand is now a statistical anomaly, what a $10M film that out-opened every blockbuster tells us about it — and how to tell whether your media budget is rent or ownership.

Hi to newcomers, this newsletter is english based due to its US distribution. Down here italian translation. Enjoy.

A year ago I thought my career was over.

Not because I had no work. Because I had no identity. For twenty years I had introduced myself through the logos on my slides — FOX, Disney. I sold attention at scale for a living. Then the slides were gone, and so, apparently, was I.

It took me a while to understand what had actually happened. My identity had been rented. It belonged to the brands I represented, and when the lease ended, it went back to the landlord.

I’m telling you this because the same thing is happening to brands themselves. They just haven’t noticed yet.

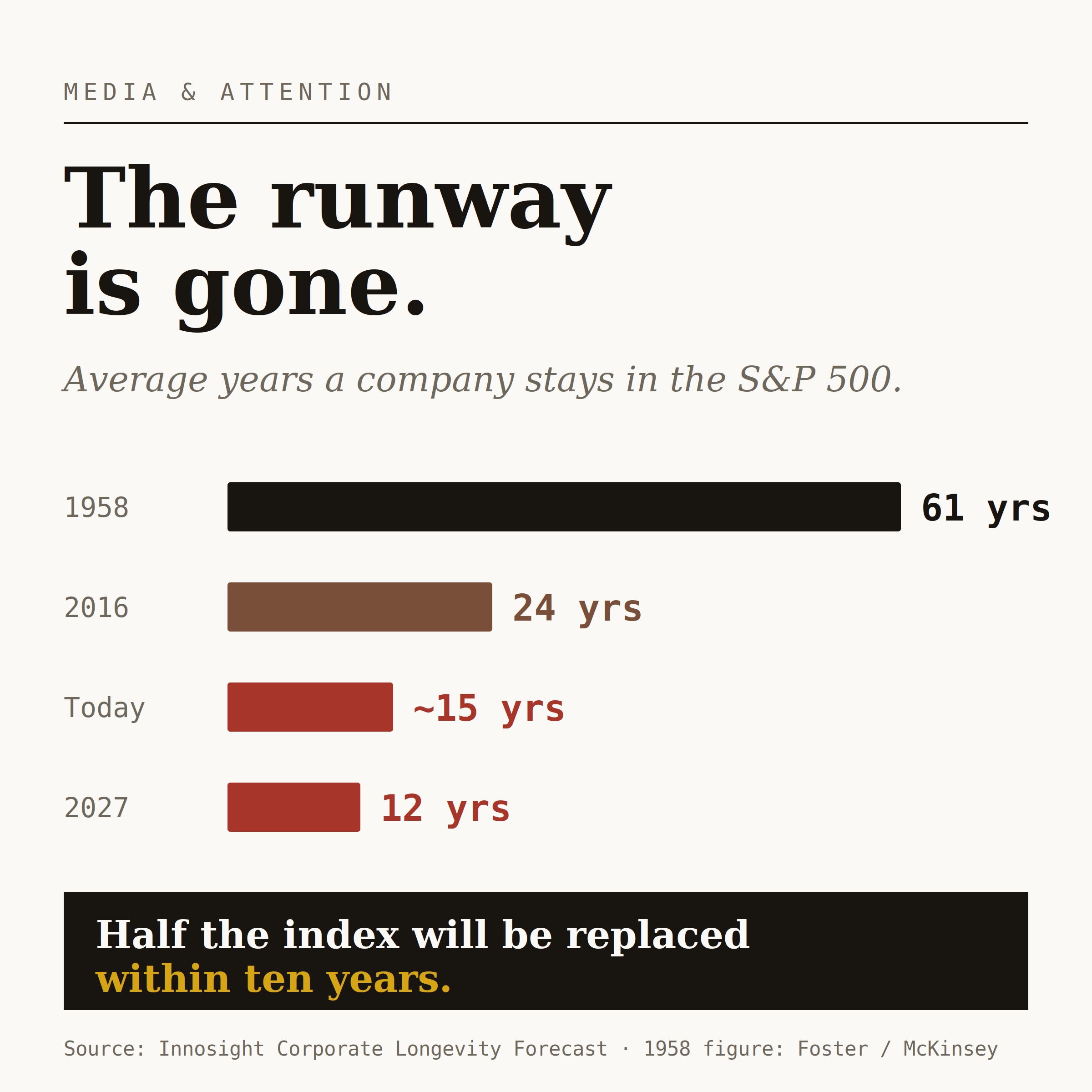

Here’s the number that should keep a CMO up at night.

The classic brand-building model — rent attention at scale, year after year, until familiarity hardens into equity — assumes you have decades. You don’t.

And while the slow model runs out of runway, something else keeps happening. It happened again two weeks ago.

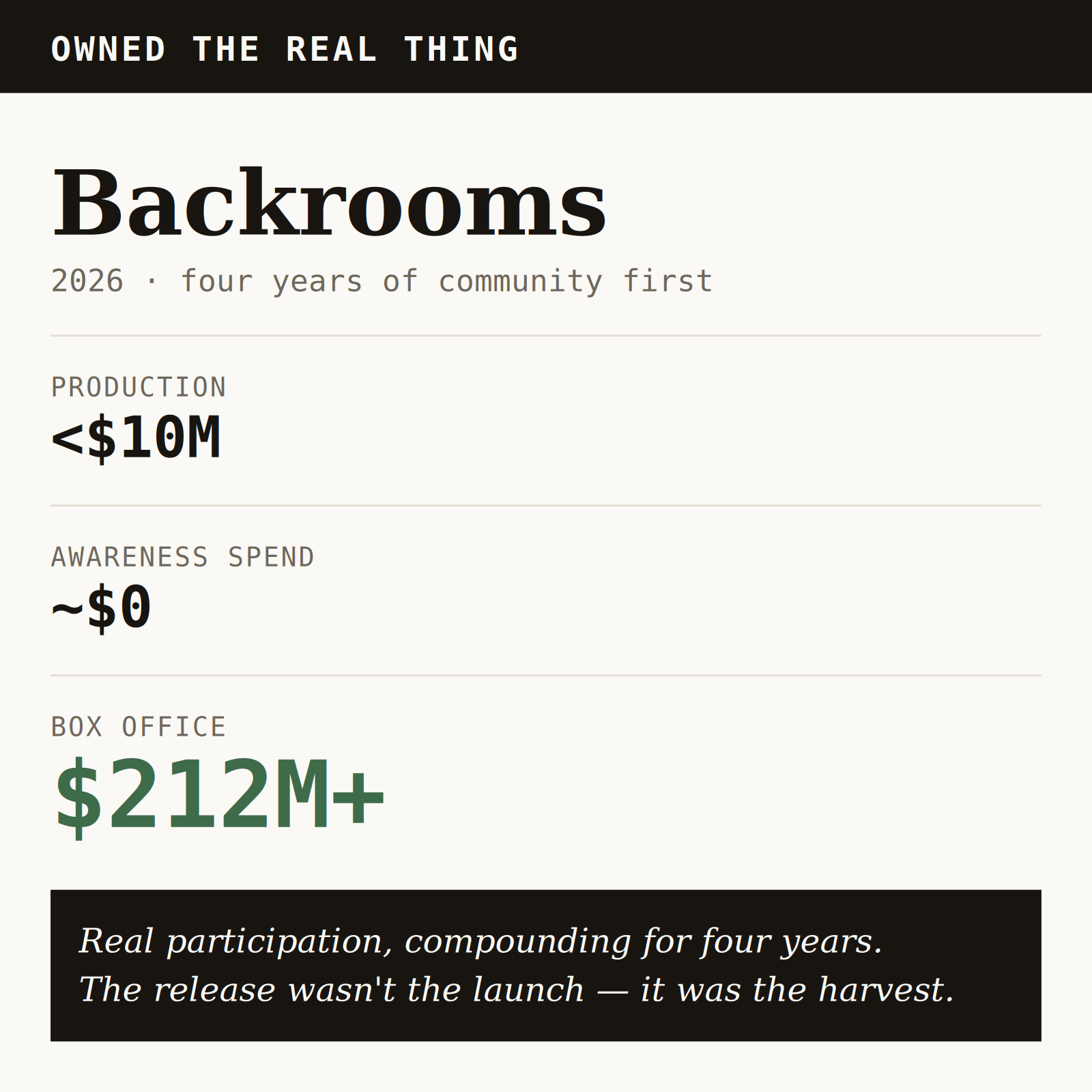

A film called Backrooms opened in late May. Budget: under $10 million. Marketing campaign: essentially none. Result: roughly $89 million domestic — A24’s biggest opening ever — directed by a twenty-year-old making his first film.

Except he wasn’t. He’d been making it for four years, on YouTube, with his audience, 190 million views at a time. Backrooms started in 2019 as internet folklore: one photo of an empty yellow office, and a community that couldn’t stop building on it. Nobody owned it, so everybody did. By the time A24 sold the first ticket, the marketing had been done — for free, by the audience, years in advance.

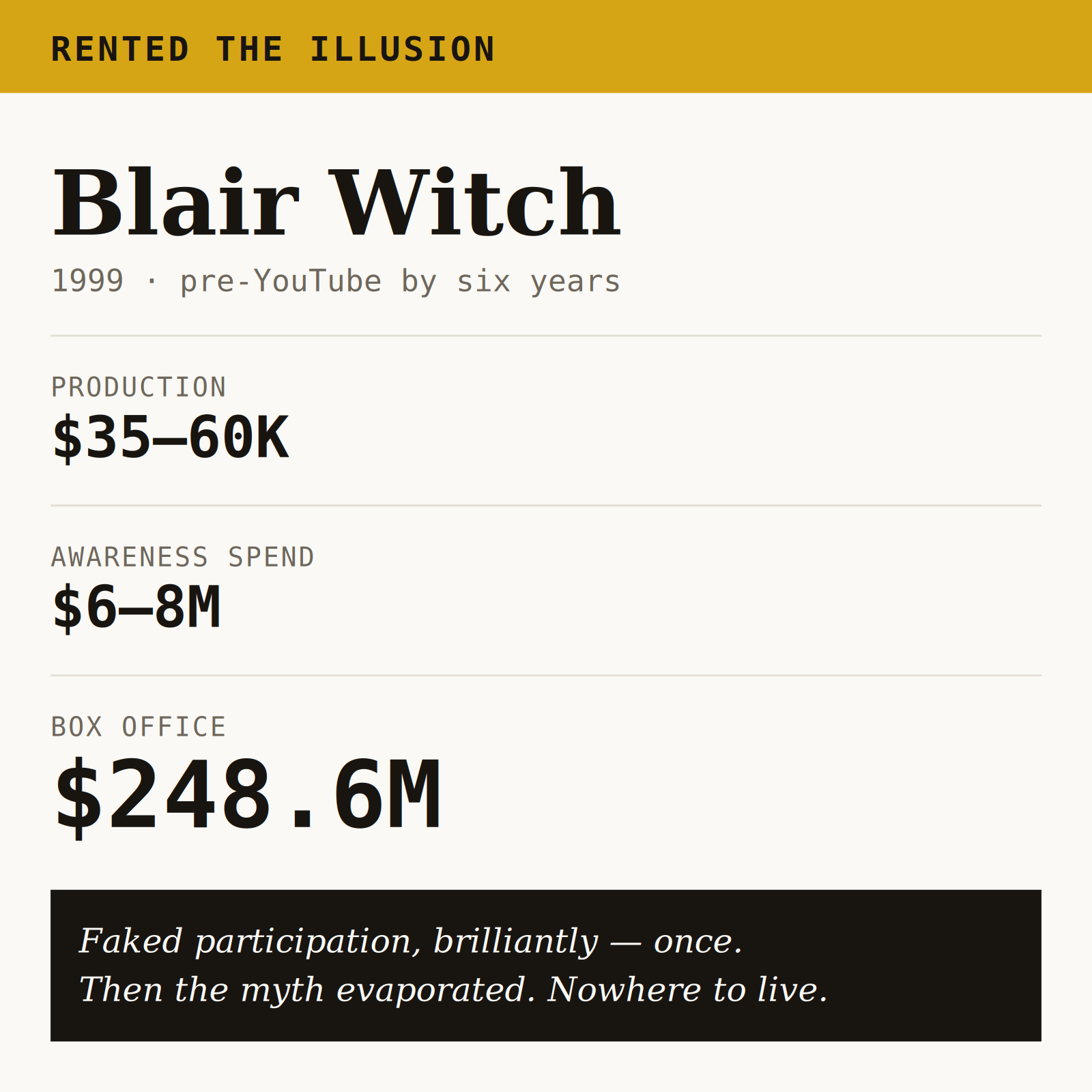

If you’re thinking The Blair Witch Project, you’re half right — and the comparison deserves a pause.

1999: three unknown filmmakers shoot a horror movie for about $60,000. The distributor builds a marketing campaign disguised as reality — a website insisting the students really disappeared, missing-person flyers handed out at Sundance — and the film grosses roughly $248 million worldwide. It was the Backrooms playbook, executed brilliantly, once.

But here’s what strikes me most, almost thirty years later: the phenomenon died right there. YouTube was six years away. There was no platform where that community could keep building, no place for the myth to live between the theater and nowhere. Blair Witch had to fake participation because real participation had no infrastructure yet. Backrooms ran the sequence in reverse: four years of real, compounding participation first — then the theatrical release as the harvest. Same trick, separated by three decades of infrastructure. One rented the illusion of a community. The other owns an actual one. And I keep asking myself: what would Blair Witch have become with YouTube underneath it?

So here is my thesis, and I’ll spend the rest of this piece earning it with numbers:

Brand cultural capital has a new generation model. It’s no longer accumulated slowly through rented attention. It’s generated fast, through participation — attention that is chosen, owned, compounding. It also decays faster, fails far more often, and cannot be bought on a rate card. I’m not here to tell you the old model is dead or to defend the new one. I’m here to help you tell the difference — because your media budget currently can’t.

I know how this story goes. I rented for twenty years. Then I had to learn to own.

TL;DR

Brand equity now has two production models: slow accumulation through rented attention, and fast generation through participation. The second is cheaper and faster — and it decays sooner.

This is a pattern, not a lottery ticket

One viral film is an anecdote. So let’s leave cinema and go to the least glamorous category imaginable: a chocolate bar.

MrBeast launched Feastables in 2022. Revenue went from $33 million that year to $96 million in 2023 to $250 million in 2024 — with $20 million in profit. Projections for 2025 sit around half a billion. It’s on shelves in more than 30,000 retail locations.

Now the detail that matters. In 2024, MrBeast’s media operation — the YouTube channel with over 100 billion lifetime views, the Amazon show — lost roughly $80 million on $246 million of revenue. The chocolate bar out-earned the most-watched channel in the history of the medium.

Read that again from a media planner’s chair. The content isn’t the product. The content is the substrate — the place where attention accumulates, freely given, years before anything is sold. The bar is just what gets attached to it. And even the bar is participatory: golden-ticket promotions turn each purchase into a lottery entry for appearing in a video. Fans aren’t buying chocolate. They’re buying a stake in the story.

The mechanism has a name in behavioral economics: the endowment effect. People defend and propagate what they helped build. Rented attention buys you reach. Participation makes the audience co-owners of the meaning — and co-owners do your marketing for you, with more credibility than any campaign you could buy. That’s why Backrooms “didn’t need marketing.” The marketing was the community.

And if two categories aren’t enough, take a third: Five Nights at Freddy’s, an indie video game built in a bedroom in 2014, whose lore was assembled collaboratively by a decade of YouTube theory channels. The 2023 film adaptation opened to $80 million — the highest-grossing horror movie of its year. The sequel, last December, opened to $63 million and passed $200 million worldwide while the rest of its studio’s slate struggled.

A creepypasta, a chocolate bar, a bedroom video game. Three categories, one engine. That’s not luck. That’s infrastructure — twenty years of YouTube maturing into an IP-generation system.

TL;DR

MrBeast’s chocolate out-earns his channel. Content isn’t the product — it’s the substrate where attention accumulates, freely given, before anything is sold.

02 · The counter-case. Same shelf, opposite destinies

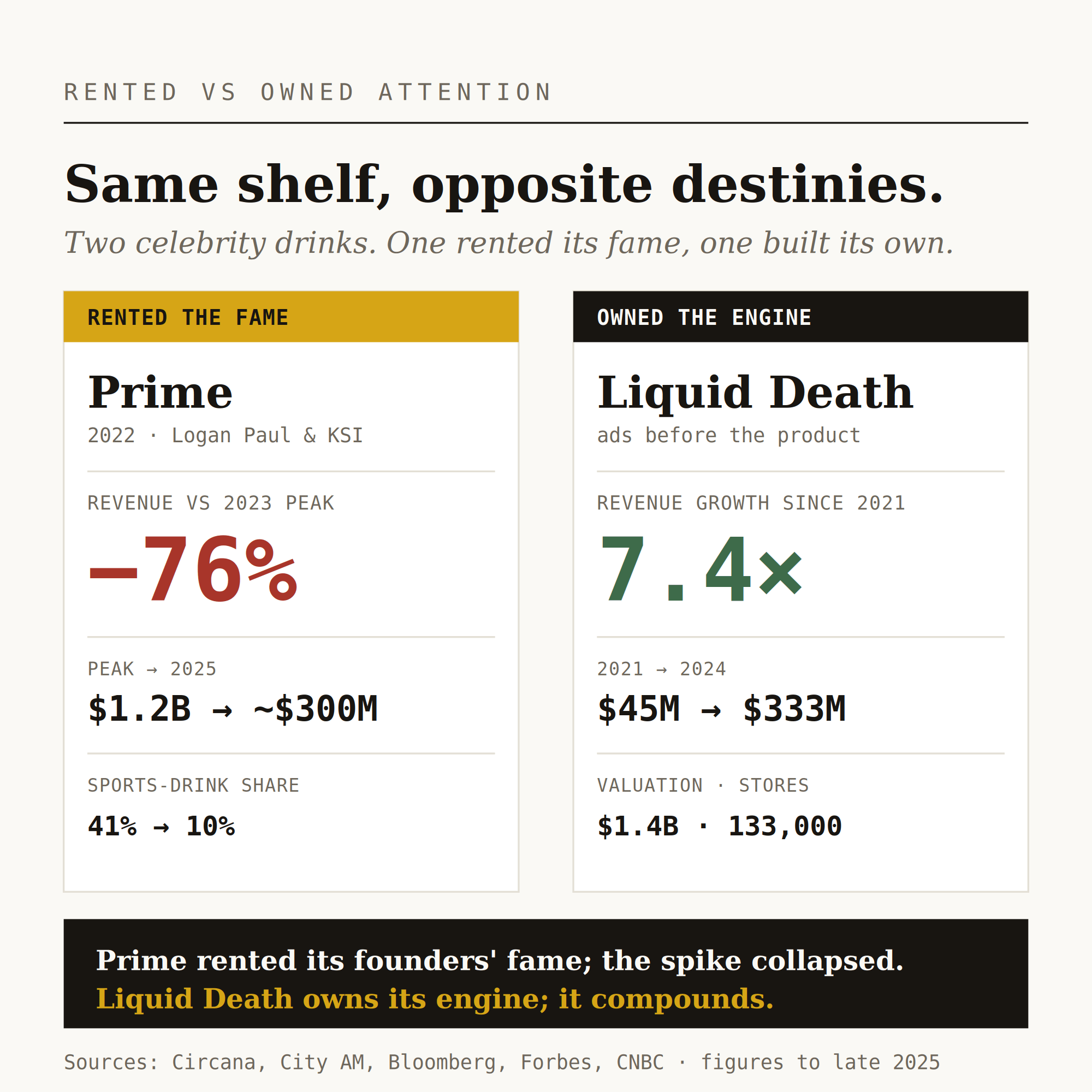

Here’s where I’m supposed to tell you the new model always wins. It doesn’t. And the cleanest proof sits in a single product category: water in a can, fronted by internet celebrities.

Case one: Prime, launched in 2022 by Logan Paul and KSI — a combined audience of 60 million subscribers. Peak: roughly $1.2 billion in global sales in 2023, a billion bottles sold in under two years, briefly outselling Gatorade at Walmart. UK retailers put anti-theft tags on individual bottles.

Then: by late 2025, revenue projections had crashed about 76 percent from peak, to around $300 million. UK revenue fell from £112 million to £33 million in a single year. Share of the sports-drink market: from 41 percent to 10. The bottles that resold for £1,200 now sit in clearance bins at 31 pence.

Case two: Liquid Death. Founder Mike Cessario ran social video ads before the product existed — he wanted to know whether the attention was real before building the company. Revenue: $45 million in 2021, $110 million, $263 million, $333 million in 2024. Valuation: $1.4 billion. 133,000 stores. Growth is decelerating — from 139 percent to 27 percent — but decelerating is not collapsing. The curve is flattening, not falling off a cliff

Same shelf. Same playbook on the surface — celebrity, content, spectacle. Opposite outcomes. Why?

Prime rented its founders’ fame. One enormous, brilliant burst of scarcity and FOMO — and when distribution killed the scarcity, the reason to buy evaporated. The attention always belonged to Logan Paul and KSI; the brand was subletting. Liquid Death owns its attention: an entertainment engine that runs continuously, a community that performs the brand (you can literally “sell your soul” on their website), an asset that compounds instead of expiring.

This is the distinction to take into your next budget meeting: rented attention versus owned attention. The first is an operating expense. The second is a capital asset.

Rented attention is reach you pay for on someone else’s inventory, and it stops the moment you stop paying. Owned attention is an audience that chose you, participates in you, and keeps working between campaigns.

And the decay rates are not the same. True brand loyalty fell to 29 percent in 2025, down five points in a year. Twenty-nine percent of consumers say they lose interest in a product as soon as it stops trending. If your brand lives on trend, it dies on schedule.

TL;DR

Rented attention is an operating expense — it stops when you stop paying. Owned attention is a capital asset — it compounds between campaigns. Prime and Liquid Death sit on the same shelf and prove the difference.

03 · The objection ”That’s Gen Z stuff” — and why it’s worse than you think

Every time I present this to a legacy-brand audience, the same hand goes up. Nice stories. Creepypastas and chocolate bars. Our customers are adults buying serious things.

Fine. Let’s look at the most adult, highest-consideration purchase a household makes: a car.

BYD — a brand most Europeans couldn’t name five years ago — sold about 2.25 million battery-electric vehicles in 2025, overtaking Tesla globally for the first time. In Europe it tripled sales and passed Tesla month after month from mid-2025, growing its EU share from 0.4 to 1.5 percent in a single year. People are handing tens of thousands of euros to a brand with zero accumulated equity in their market.

Or look at the most mainstream, most mature audience there is: grocery shoppers. Private label has reached a record 50 percent unit share across Europe’s six biggest grocery markets — 59 percent in Spain, 52 percent in the UK and Germany, 36 percent and climbing in Italy. Hundreds of billions of euros that used to flow through “irreplaceable” brand equity, gone to the retailer’s own label.

Now, intellectual honesty — because this is where most takes on this subject cheat. BYD and private label are not participatory phenomena. Nobody is co-creating a myth around store-brand pasta. These are value disruptions: better price, good-enough or better product.

But that’s exactly why they belong in this argument. Legacy brands are being squeezed by two convergent forces, not one. From below, participatory generation — Backrooms, MrBeast, Liquid Death — building cultural capital faster than any media plan can. From the side, value disruption — BYD, private label — proving that twenty years of accumulated equity is a much shallower moat than the balance sheet assumes. It can be crossed in three years by anyone with a better offer.

The old mid-market brand — built on rented mass attention, defended by familiarity — is caught between the two. One force you can answer with media strategy. The other you can’t: no amount of owned attention saves you if the retailer’s label is genuinely better value. That’s an operations problem wearing a marketing costume, and I won’t sell you communication as the cure. Knowing which force is eating you is the first real decision.

TL;DR

Legacy brands face two convergent forces: participatory generation from below, value disruption from the side. Only one of them can be answered with media strategy. Diagnose before you spend.

04 · The defense. What a legacy brand can actually do

If the disruption is participatory — the one media strategy can answer — there are three moves. Each comes with a failure mode, because that’s the part the conference-keynote version always omits.

First: invert the stack. The legacy model makes the product first and rents media to push it. The new model builds an attention asset first and attaches products to it. The provocation, stated plainly: your media budget is currently an operating expense that rents decaying attention; part of it should become capital expenditure in an attention asset you own. The constraint: this is a multi-year commitment, and corporate finance is built to treat media as a cost to optimize down, not an asset to capitalize. If your CFO can’t fund patience, you can’t play.

Second: open participation — on the right layer. You cannot make the core utility of a serious product co-creatable; nobody crowdsources brake systems. But you can open a governed channel on the meaning layer. LEGO Ideas has done it for nearly two decades: fans design sets, the community votes, winners go into production with the creator’s name on the box. Real participation, real governance. The constraint: it only works if you genuinely cede a slice of authorship. Staged participation — the rigged contest, the domesticated UGC campaign — gets detected instantly and produces the opposite of trust.

Third: spin off, and accept the math. Your accumulated equity is both your asset and your prison: too much downside to let the mother brand play an open, high-variance game. So you separate small bets with no equity to protect, firewalled so a failure doesn’t contaminate the house. This is the organizational form of an uncomfortable truth: participatory phenomena follow a power-law. For every Backrooms there are ten thousand dead memes. You cannot engineer the hit; you can only afford many cheap attempts. The constraint is governance: the parent almost never resists the urge to control, and “owned by Megacorp” can kill the very authenticity the spin-off was built to find.

TL;DR

Three moves: invert the stack, open the meaning layer, spin off the variance. Each fails exactly where corporate governance usually wins.

05 · The real obstacle. It isn’t strategy

Notice what these three moves have in common. None of them is conceptually difficult. Invert the stack, cede some authorship, tolerate dead bets, fund patience. Any strategy team can write that deck by Friday.

What they share is that each one violates the operating system of a legacy organization. Quarterly media budgets. Brand guidelines as legal documents. Risk committees. The institutional reflex that authority comes with the logo. I spent twenty years inside that system; I know its immune response intimately. It rejects precisely the antibodies that would save it.

So the question I’d leave in your next budget meeting isn’t “should we do a TikTok.”

It’s this: how much of your media budget is rent, and how much is ownership? And who, in your governance, actually has the mandate to build instead of lease?

A year ago I had to answer that question about my own career. The lease was over. Building was slower, lonelier, and statistically unreasonable. Twelve months later, the attention I own — small as it is — brings me clients the rented kind never did.

Brands are about to learn the same lesson. The only choice is whether to learn it before the lease runs out.

___________

Sources: Innosight Corporate Longevity Forecast · Box Office Mojo / Variety (Backrooms, FNAF) · Bloomberg / Fortune / Sacra (Feastables, Liquid Death) · Circana / City AM (Prime) · ACEA / JATO (BYD) · Circana / PLMA (private label) · Emarsys-SAP loyalty research 2025.

__________

L’attenzione in affitto è un asset che si scioglie. Lo so — la mia l’ho persa.

Un anno fa pensavo che la mia carriera fosse finita.

Non perché fossi senza lavoro. Perché non avevo più un’identità. Per vent’anni mi ero presentato attraverso i loghi sulle mie slide — FOX, Disney. Vendere attenzione su larga scala era il mio mestiere. Poi le slide sono sparite, e con loro, a quanto pareva, anch’io.

Ci ho messo un po’ a capire cosa fosse successo davvero. La mia identità era stata in affitto. Apparteneva ai brand che rappresentavo, e quando il contratto è scaduto è tornata al proprietario.

Te lo racconto perché ai brand sta succedendo la stessa cosa. Solo che non se ne sono ancora accorti.

Ecco il numero che dovrebbe tenere sveglio un CMO la notte. Nel 1958 un’azienda restava nell’indice S&P 500 in media 61 anni. Oggi siamo intorno ai quindici, in discesa verso dodici, secondo la ricerca di Innosight sulla longevità aziendale. Metà dell’indice si rinnoverà entro un decennio. Il modello classico di brand building — affittare attenzione su larga scala, anno dopo anno, finché la familiarità si indurisce in equity — presuppone che tu abbia decenni davanti. Non li hai.

E mentre il modello lento esaurisce la pista, succede qualcos’altro. È successo di nuovo due settimane fa.

A fine maggio è uscito un film, Backrooms. Budget: sotto i 10 milioni di dollari. Campagna marketing: praticamente nessuna. Risultato: 81 milioni di dollari di apertura solo negli Stati Uniti — il più alto nella storia di A24, il triplo del record precedente dello studio — e oltre 212 milioni nel mondo in dieci giorni, il film più redditizio mai distribuito da A24, diretto da un ventenne al suo primo film. Il più giovane regista di sempre ad aprire un film al primo posto.

Solo che non era il primo. Lo costruiva da quattro anni, su YouTube, con il suo pubblico, 190 milioni di visualizzazioni alla volta. Backrooms nasce nel 2019 come folklore di internet: la foto di un ufficio giallo e vuoto, e una community che non smetteva di costruirci sopra. Nessuno lo possedeva, quindi lo possedevano tutti. Quando A24 ha venduto il primo biglietto, il marketing era già stato fatto — gratis, dal pubblico, con anni di anticipo.

Se stai pensando a The Blair Witch Project, hai ragione a metà — e il confronto merita una pausa. 1999: tre registi sconosciuti girano un horror con un budget tra i 35.000 e i 60.000 dollari; il film finito, dopo la post-produzione, costa qualche centinaio di migliaia. Artisan lo compra al Sundance per poco più di un milione, costruisce una campagna travestita da realtà — un sito che insisteva che gli studenti fossero spariti davvero, volantini di persone scomparse distribuiti al festival — e spende, secondo le stime, 6-8 milioni di dollari solo di marketing domestico. Il film incassa 248,6 milioni nel mondo. Era il copione di Backrooms, eseguito alla perfezione, una volta sola.

Ma ecco quello che mi colpisce di più, quasi trent’anni dopo: il fenomeno è morto lì. A YouTube mancavano sei anni. Non c’era una piattaforma dove quella community potesse continuare a costruire, nessun posto dove il mito potesse vivere tra la sala e il nulla. Blair Witch ha dovuto fingere la partecipazione perché la partecipazione vera non aveva ancora un’infrastruttura. Il mito ha toccato il picco al botteghino ed è evaporato. Backrooms ha percorso la sequenza al contrario: prima quattro anni di partecipazione vera, che fa compounding — poi l’uscita al cinema come raccolto. Stesso trucco, separati da tre decenni di infrastruttura. Uno affittava l’illusione di una community. L’altro ne possiede una vera. E continuo a chiedermelo: cosa sarebbe diventato Blair Witch con YouTube sotto?

Quindi ecco la mia tesi, e passerò il resto del pezzo a guadagnarmela coi numeri:

Il capitale culturale del brand ha un nuovo modello di generazione. Non si accumula più lentamente attraverso attenzione affittata. Si genera in fretta, attraverso la partecipazione — attenzione scelta, di proprietà, che fa compounding. Decade anche più in fretta, fallisce molto più spesso, e non si compra a listino. Non sono qui per dirti che il vecchio modello è morto, né per difendere quello nuovo. Sono qui per aiutarti a distinguerli — perché il tuo budget media, oggi, non ci riesce.

So come va a finire questa storia. Ho affittato per vent’anni. Poi ho dovuto imparare a possedere.

È un pattern, non un biglietto della lotteria

Un film virale è un aneddoto. Allora lasciamo il cinema e andiamo nella categoria meno glamour che esista: una barretta di cioccolato.

MrBeast ha lanciato Feastables nel 2022. I ricavi sono passati da 33 milioni quell’anno a 96 milioni nel 2023 a 250 milioni nel 2024 — con 20 milioni di utile. Le proiezioni per il 2025 si aggirano sul mezzo miliardo. È sugli scaffali di oltre 30.000 punti vendita.

Ora il dettaglio che conta. Nel 2024 la divisione media di MrBeast — il canale YouTube con oltre 100 miliardi di visualizzazioni storiche, lo show su Amazon — ha perso circa 80 milioni su 246 di ricavi. La barretta di cioccolato ha guadagnato più del canale più visto nella storia del mezzo.

Rileggilo dalla sedia di un media planner. Il contenuto non è il prodotto. Il contenuto è il substrato — il luogo dove l’attenzione si accumula, donata, anni prima che ci sia qualcosa da vendere. La barretta è solo ciò che ci si attacca. E persino la barretta è partecipata: le promozioni “golden ticket” trasformano ogni acquisto in un biglietto della lotteria per comparire in un video. I fan non comprano cioccolato. Comprano una quota nella storia.

Il meccanismo ha un nome in economia comportamentale: l’effetto dotazione. Le persone difendono e diffondono ciò che hanno contribuito a costruire. L’attenzione affittata ti compra reach. La partecipazione rende il pubblico comproprietario del significato — e i comproprietari fanno il tuo marketing al posto tuo, con più credibilità di qualsiasi campagna tu possa comprare. Ecco perché Backrooms “non aveva bisogno di marketing”. Il marketing era la community.

E se due categorie non bastano, prendine una terza: Five Nights at Freddy’s, un videogioco indie costruito in una cameretta nel 2014, la cui lore è stata assemblata collettivamente da dieci anni di canali YouTube di teorie. L’adattamento cinematografico del 2023 ha aperto a 80 milioni — l’horror col maggiore incasso dell’anno. Il sequel, lo scorso dicembre, ha aperto a 63 milioni e superato i 200 milioni nel mondo mentre il resto del listino dello stesso studio arrancava.

Una creepypasta, una barretta di cioccolato, un videogioco fatto in cameretta. Tre categorie, un solo motore. Non è fortuna. È infrastruttura — vent’anni di YouTube maturati in un sistema di generazione di IP.

Stesso scaffale, destini opposti

È qui che dovrei dirti che il nuovo modello vince sempre. Non è così. E la prova più pulita sta in un’unica categoria di prodotto: acqua in lattina, con la faccia di celebrità di internet.

Caso uno: Prime, lanciato nel 2022 da Logan Paul e KSI — un pubblico combinato di 60 milioni di iscritti. Picco: circa 1,2 miliardi di vendite globali nel 2023, un miliardo di bottiglie in meno di due anni, per un attimo più di Gatorade da Walmart. Nel Regno Unito i rivenditori mettevano l’antitaccheggio sulle singole bottiglie.

Poi: entro fine 2025 le proiezioni di ricavi erano crollate di circa il 76% dal picco, a circa 300 milioni. Nel Regno Unito i ricavi sono scesi da 112 a 33 milioni di sterline in un solo anno. Quota nel mercato degli sport drink: dal 41% al 10%. Le bottiglie che si rivendevano a 1.200 sterline ora stanno nei cestoni delle svendite a 31 penny.

Le cause su sostanze chimiche e contenuto di caffeina si sono accumulate dal 2023 — ma erano acceleranti, non il motore. La vulnerabilità più profonda era strutturale: l’attenzione affittata non ha fiducia accumulata per assorbire uno shock. Coca-Cola è sopravvissuta a decenni di polemiche su zucchero e plastica; Prime non aveva fedeltà stratificata da spendere, solo trend. E affittare attenzione da una persona significa ereditarne l’intero profilo di rischio — il brand era ostaggio della reputazione dei suoi fondatori, controversie passate incluse. L’attenzione di proprietà distribuisce il rischio su una community. Quella affittata lo concentra in un unico punto di rottura.

Caso due: Liquid Death. Il fondatore Mike Cessario ha mandato pubblicità video sui social prima che il prodotto esistesse — voleva sapere se l’attenzione fosse reale prima di costruire l’azienda. Ricavi: 45 milioni nel 2021, 110, 263, 333 milioni nel 2024. Valutazione: 1,4 miliardi. 133.000 negozi. La crescita rallenta — dal 139% al 27% — ma rallentare non è crollare. La curva si appiattisce, non precipita.

Stesso scaffale. Stesso copione in superficie — celebrità, contenuto, spettacolo. Esiti opposti. Perché?

Prime ha affittato la fama dei suoi fondatori. Un’unica, geniale esplosione di scarsità e FOMO — e quando la distribuzione ha ucciso la scarsità, la ragione d’acquisto è evaporata. L’attenzione è sempre appartenuta a Logan Paul e KSI; il brand era in subaffitto. Liquid Death possiede la sua attenzione: un motore di intrattenimento che gira di continuo, una community che mette in scena il brand (sul loro sito puoi letteralmente “vendere l’anima”), un asset che fa compounding invece di scadere.

È questa la distinzione che voglio tu porti al prossimo budget meeting: attenzione in affitto contro attenzione di proprietà. L’attenzione affittata è reach che paghi sull’inventory di qualcun altro, e si ferma nel momento in cui smetti di pagare. L’attenzione di proprietà è un pubblico che ti ha scelto, che partecipa, e che continua a lavorare tra una campagna e l’altra. La prima è un costo operativo. La seconda è un asset di capitale.

E i tassi di decadimento non sono uguali. La fedeltà che i brand credono di avere è in larga parte del tipo fragile — da punti, sconti, abitudine: secondo l’indice Emarsys 2025, solo il 29% dei consumatori dichiara un attaccamento reale a un marchio, e il resto evapora nel momento in cui arriva un’alternativa più economica o più di moda. Se il tuo brand vive di trend, muore secondo calendario.

“È roba da Gen Z” — l’obiezione, e perché è peggio di quanto pensi

Ogni volta che presento questa tesi a un’audience di brand legacy, si alza sempre la stessa mano. Belle storie. Creepypasta e barrette di cioccolato. I nostri clienti sono adulti che comprano cose serie.

Bene. Prendiamo l’acquisto più adulto e ad alto coinvolgimento che una famiglia faccia: l’auto.

BYD — un marchio che cinque anni fa la maggior parte degli europei non sapeva nominare — ha venduto circa 2,25 milioni di auto elettriche nel 2025, superando Tesla a livello globale per la prima volta. In Europa ha triplicato le vendite e ha superato Tesla mese dopo mese dalla metà del 2025, portando la sua quota UE dallo 0,4% all’1,5% in un solo anno. Le persone consegnano decine di migliaia di euro a un marchio con zero equity accumulata nel loro mercato.

Oppure guarda l’audience più mainstream e più matura che esista: chi fa la spesa. La marca del distributore ha raggiunto un record del 50% di quota a volume nei sei maggiori mercati grocery europei — 59% in Spagna, 52% nel Regno Unito e in Germania, 36% e in crescita in Italia. Centinaia di miliardi di euro che un tempo passavano per l’equity “insostituibile” del brand, finiti alla marca del retailer.

Ora, onestà intellettuale — perché è qui che la maggior parte delle analisi su questo tema bara. BYD e private label non sono fenomeni partecipativi. Nessuno co-costruisce un mito attorno alla pasta a marchio del distributore. Sono disruption di valore: prezzo migliore, prodotto buono o migliore.

Ma è proprio per questo che appartengono a questo discorso. I brand legacy sono schiacciati da due forze convergenti, non una. Dal basso, la generazione partecipata — Backrooms, MrBeast, Liquid Death — che costruisce capitale culturale più in fretta di qualsiasi piano media. Di lato, la disruption di valore — BYD, private label — che dimostra come vent’anni di equity accumulata siano un fossato molto più basso di quanto creda il bilancio. Si attraversa in tre anni, da chiunque abbia un’offerta migliore.

Il vecchio brand di fascia media — costruito su attenzione di massa affittata, difeso dalla familiarità — è preso in mezzo tra le due. Una forza la puoi affrontare con la strategia media. L’altra no: nessuna quantità di attenzione di proprietà ti salva se la marca del retailer vale davvero di più. Quello è un problema di operations travestito da problema di marketing, e non ti venderò la comunicazione come cura. Capire quale delle due ti sta mangiando è la prima decisione vera.

Cosa può fare davvero un brand legacy

Se la disruption è partecipativa — quella a cui la strategia media può rispondere — ci sono tre mosse. Ognuna con il suo punto di rottura, perché è la parte che la versione da keynote omette sempre.

Primo: invertire lo stack. Il modello legacy fa prima il prodotto e affitta media per spingerlo. Il modello nuovo costruisce prima un asset di attenzione e ci appende i prodotti. Non è nemmeno una novità: Michelin l’aveva capito nel 1900, quando un’azienda di pneumatici pubblicò una guida che diventò l’autorità mondiale sui ristoranti — un asset di contenuto sopravvissuto a ogni campagna pubblicitaria mai fatta nella categoria, e che vende ancora pneumatici facendo venire alla gente voglia di guidare da qualche parte. La provocazione, detta chiara: il tuo budget media oggi è una spesa operativa che affitta attenzione in decadenza; una parte dovrebbe diventare spesa in conto capitale su un asset di attenzione di tua proprietà.

Per essere chiari, questo non è un argomento contro la pubblicità. La reach a pagamento fa ancora ciò che nient’altro fa — mantiene la mental availability, difende l’equity a scaffale, raggiunge persone che la tua community non toccherà mai. L’argomento è contro la pubblicità come unica voce: 100% affitto, 0% proprietà. E sì, i contabili obietteranno che il marketing non può stare a bilancio con gli standard attuali. Va bene — trattalo come capex nella governance, non nella contabilità: un orizzonte pluriennale, un responsabile che risponde dell’asset, una mentalità da ammortamento invece che da campagna. Il vincolo resta: la finanza aziendale è costruita per trattare il media come un costo da ottimizzare al ribasso. Se il tuo CFO non sa finanziare la pazienza, non puoi giocare questa partita.

Secondo: aprire la partecipazione — sul layer giusto. Non puoi rendere co-costruibile l’utilità core di un prodotto serio; nessuno fa crowdsourcing degli impianti frenanti. Ma puoi aprire un canale governato sul layer del significato. LEGO Ideas lo fa da quasi vent’anni: i fan progettano i set, la community vota, i vincitori vanno in produzione col nome del creatore sulla scatola. Partecipazione vera, governance vera. Il vincolo: funziona solo se cedi davvero una fetta di autorialità. La partecipazione recitata — il concorso pilotato, la campagna UGC addomesticata — viene fiutata all’istante e produce l’opposto della fiducia.

Terzo: scorporare, e accettare la matematica. La tua equity accumulata è insieme il tuo asset e la tua prigione: troppo downside per lasciare che il brand madre giochi una partita aperta e ad alta varianza. Quindi separi piccole scommesse senza equity da proteggere, isolate da un firewall così che un fallimento non contamini la casa madre. È la forma organizzativa di una verità scomoda: i fenomeni partecipativi seguono una power-law. Per ogni Backrooms ci sono diecimila meme morti. Non puoi ingegnerizzare il successo; puoi solo permetterti molti tentativi a basso costo. Il vincolo è la governance: il genitore quasi mai resiste all’impulso di controllare, e “posseduto da una multinazionale” può uccidere proprio l’autenticità che lo scorporo doveva trovare.

L’ostacolo vero non è la strategia

Nota cosa hanno in comune queste tre mosse. Nessuna è concettualmente difficile. Invertire lo stack, cedere un po’ di autorialità, tollerare le scommesse morte, finanziare la pazienza. Qualsiasi team strategico scrive quella presentazione entro venerdì.

Ciò che le accomuna è che ognuna viola il sistema operativo di un’organizzazione legacy. Budget media trimestrali. Brand guideline come documenti legali. Comitati di rischio. Il riflesso istituzionale per cui l’autorità arriva col logo. Ho passato vent’anni dentro quel sistema; ne conosco intimamente la risposta immunitaria. Rigetta proprio gli anticorpi che lo salverebbero.

Quindi la domanda che lascerei al tuo prossimo budget meeting non è “facciamo un TikTok?”.

È questa: quanta parte del tuo budget media è affitto, e quanta è proprietà? E chi, nella tua governance, ha davvero il mandato di costruire invece di noleggiare?

Un anno fa ho dovuto rispondere a quella domanda sulla mia carriera. Il contratto d’affitto era finito. Costruire era più lento, più solitario e statisticamente irragionevole. Dodici mesi dopo, l’attenzione che possiedo — per quanto piccola — mi porta clienti che quella affittata non mi ha mai portato.

I brand stanno per imparare la stessa lezione. L’unica scelta è se impararla prima che scada il contratto.

Fonti e dati

Permanenza nell’S&P 500: Innosight, Corporate Longevity Forecast (aggiornamento 2021). Incassi Backrooms: Deadline e Variety, giugno 2026 (dati all’8 giugno 2026 — film ancora in sala). Blair Witch Project: The Hollywood Reporter (acquisizione Artisan e spesa marketing); Box Office Mojo (incassi). Feastables / Beast Industries: dati aziendali riportati da Bloomberg e Business Insider, 2025. Prime Hydration: dati retail Circana e proiezioni aziendali riportati da City AM e Bloomberg; dettagli sulle cause da atti dei tribunali distrettuali USA (N.D. Cal. e S.D.N.Y.) riportati da Reuters e USA Today. Liquid Death: ricavi e round di finanziamento dichiarati dall’azienda, riportati da Forbes e CNBC. Five Nights at Freddy’s: Box Office Mojo; Deadline. BYD Europa: report vendite aziendali; dati immatricolazioni JATO Dynamics e ACEA, 2025. Marca del distributore: PLMA International e Circana, Private Label in Western Europe 2025; NIQ. Fedeltà al brand: SAP Emarsys Customer Loyalty Index 2025; McKinsey & Company, State of the Consumer 2025.